This Too Shall Pass & The Dark Side of the Moon

Good morning, all,

I wasn’t 100% sure about a newsletter on Good Friday. I guess, I’ve sent them out on a Saturday before, so this is somewhat similar. For those of you having a more relaxing day, I hope I've not disturbed it too much. I figured that if I left things until Tuesday, there was a very good chance that the references to market movements could be significantly eclipsed by events, given how everything is going.

So here we are. Where to even start.

March was - and I think I'm possibly downplaying it here - quite a month. A war in the Middle East, with oil prices doing things we haven't seen since 2022. Global stock markets having what can only be described as “a moment”. Astronauts heading to the moon for the first time in over 50 years. And the small matter of the UK tax year quietly slipping away, to be replaced by a shiny new one.

On that last point: we are right on the cusp of the 2026/27 tax year as I write this. If you pick this up after Sunday, that changeover has already happened - your ISA allowances, your pension allowances, and a host of other annual limits have refreshed. We will, naturally, be touching on all of this with all clients during your annual planning meetings. But if you'd like to get ahead of the curve - or simply to start the new tax year on the front foot – please do contact me in your usual fashion.

Now. The astronauts. As I type these words, a four-person crew is on a 10-day voyage around the moon aboard NASA's Artemis II - the first crewed lunar mission since 1972. An extraordinary thing.

What do you think will rise faster: their rocket, or the price of petrol? Place your bets, ladies and gentlemen.

On a personal front, March saw our first family ski trip, in Soldeu in Andorra. A brilliant time had by all. Our eldest took to skiing as though he'd been secretly practising in the back garden for months; scooting down the slopes and will quite evidently be better than his old man before long.

Right then. Let's get into it.

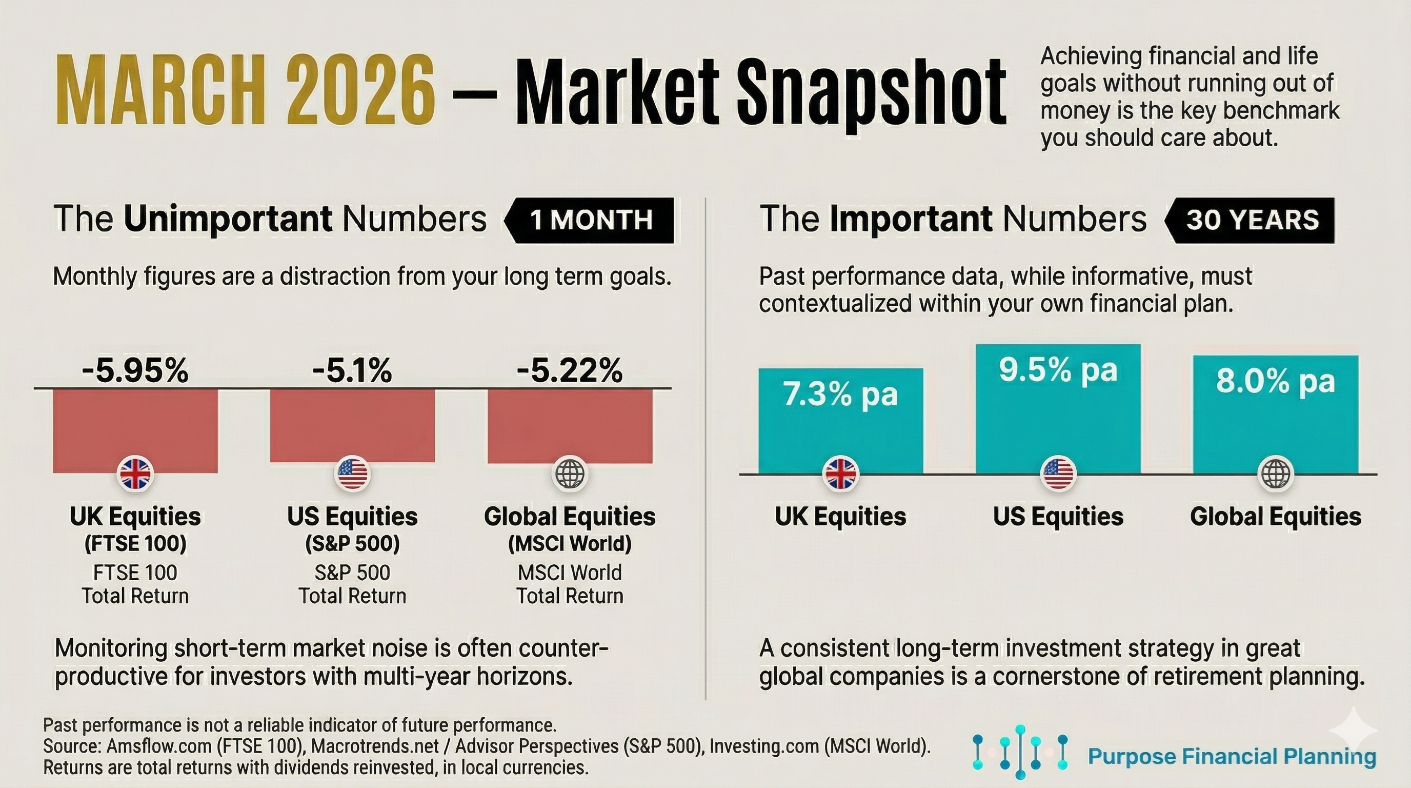

Monthly Market Visuals

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Stay in Your Seat

Since the outbreak of the conflict in Iran at the end of February, global markets have been a wee bit rattled. Somewhat upset. The S&P 500 fell by just over 5% in March alone, posting its worst quarterly performance since 2022. The Nasdaq entered correction territory. Brent crude surged above $100 a barrel for the first time in years (and seems to keep going), and prices at the pump are merciless. Airlines have warned of higher fares, or no fuel. Inflation, just when the Bank of England thought it might be getting somewhere, is back on the agenda. The financial media - never ones to let a crisis go to waste - have made the most of every twist.

And yet the advice is exactly the same as it was a year ago when I wrote about the tariff-driven volatility of spring 2025. [That piece is here if you'd like a reminder. The message then stands just as firmly now.

So, consider this a brief reprise, with a few things I want to put on record clearly.

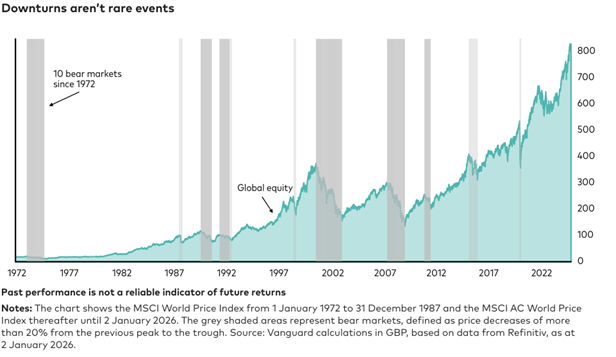

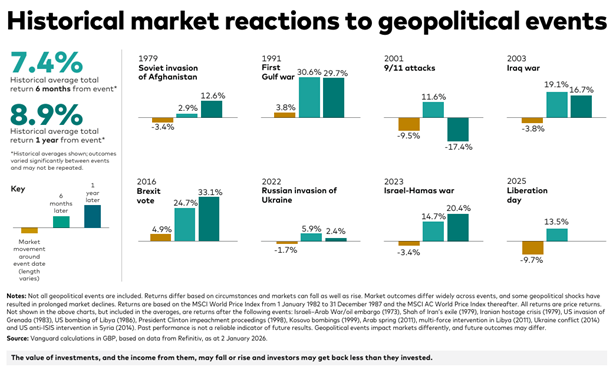

We have been here before

Geopolitical shocks - wars, oil embargoes, pandemics, financial crashes - have rattled markets throughout living memory and well beyond it. According to analysis by Stock Trader's Almanac of 17 major geopolitical incidents since 1939, the S&P 500 posted an average gain of nearly 3% in the 12 months following each initial shock.

That is not a promise - past performance is not a reliable indicator of future performance - but it is history, and history carries weight.

The companies that make up your global portfolio have navigated the 1973 oil crisis, the Gulf War, the dotcom crash, the global financial crash of 2008, Brexit, a worldwide pandemic, and a tariff war. Every single time, markets have recovered.

Every. Single. Time.

The oil shock will likely be temporary

Every previous disruption to energy markets has eventually resolved - either through negotiation, through adaptation, or through the relentless ingenuity of the companies and individuals affected. Higher oil prices are painful in the short term.

They are also a powerful incentive to find alternatives, accelerate efficiencies, and reroute supply chains. The world does not sit still.

The danger is not the market. It's the behaviour

The investors who have suffered most across history have not been the ones who stayed in their seats during downturns.

They are the ones who panicked, sold, locked in their losses, and missed the recovery. Timing the market - getting out before the bottom and back in before the bounce - is a strategy that has ended more financial plans than any war or recession ever managed on its own.

If your circumstances haven't changed, your financial plan hasn't changed. If your financial plan hasn't changed, your portfolio shouldn't either.

And if you happen to have surplus cash sitting idle - cash that isn't earmarked for anything in the next five years or so - then this kind of moment has historically been among the better times to put it to work. You are buying stakes in the world's great businesses at a discount. I appreciate that requires a particular kind of fortitude when every headline is telling you to panic. But the arithmetic doesn't change because the news is bad.

This stock market is the only type of discounted sale where, rather than filling their boots, people flee for the door.

This section is for information purposes only and does not constitute financial advice. Past performance is not a reliable indicator of future performance. The value of investments can fall as well as rise, and you may not get back the full amount invested. Investing in shares should be regarded as a long-term investment.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

As always, if you'd like to talk anything through, you know where I am.

A Word of Warning

On a rather different note - and something I feel I really should flag, although I am a very late to the party - I want to draw your attention to a piece of investigative work published last month that is, frankly, superb.

Dan Neadle and the team at Tax Policy Associates have published a truly mind-boggling investigation into a firm called MP Estate Planning.

If you have an elderly parent, a sibling, or indeed anyone in your wider circle who might conceivably have come across this firm on social media - which has been their primary hunting ground, quelle surprise - it is worth knowing about.

The short version: MP Estate Planning has been running an aggressive online campaign targeting elderly homeowners with promises of avoiding inheritance tax, care home fees, divorce claims, and creditors - all by placing assets into a trust. Their founder, one Mike Pugh, has claimed on video to be a "tax lawyer" and an "estate planning lawyer". According to the Tax Policy Associates research, he is neither.

It is a cracking read. Imagine if Taggart was a report instead of a show, and concerned with dodgy tax schemes rather than crime, and you get the idea.

Why do I raise this? Because this kind of firm doesn't announce itself as a scam. The pitch is emotionally loaded, as these sorts of things often are, and it targets people with very legitimate concerns about their estate. Those concerns are real. The solutions being sold are not.

Not something I really need to tell this audience, but more for your peers and those around you - always speak to a qualified professional before signing anything.

Please note: The FCA does not regulate inheritance tax planning or trust advice. Any planning should be based on qualified legal and tax advice specific to your individual circumstances. Taxation legislation may change.

Market Concentration - Not Always a Bad Thing?

I know I've previously and recently discussed the concept of market concentration, so I won't go over this again too much. I did want to highlight this superb data resource that someone has kindly put together, communicating that more often than not the overall growth in the stock market has been driven by a small number of firms.

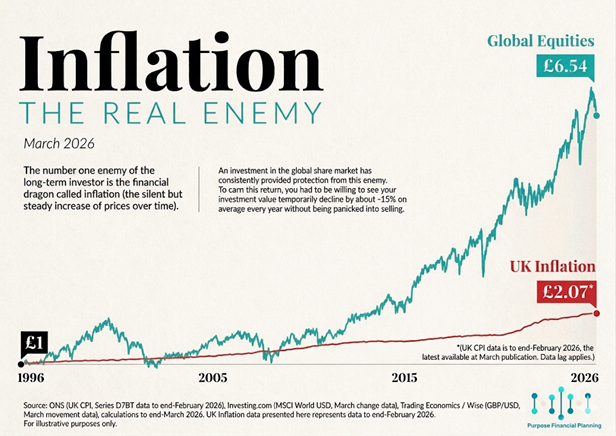

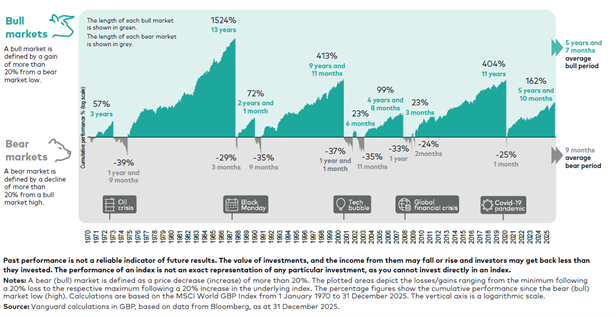

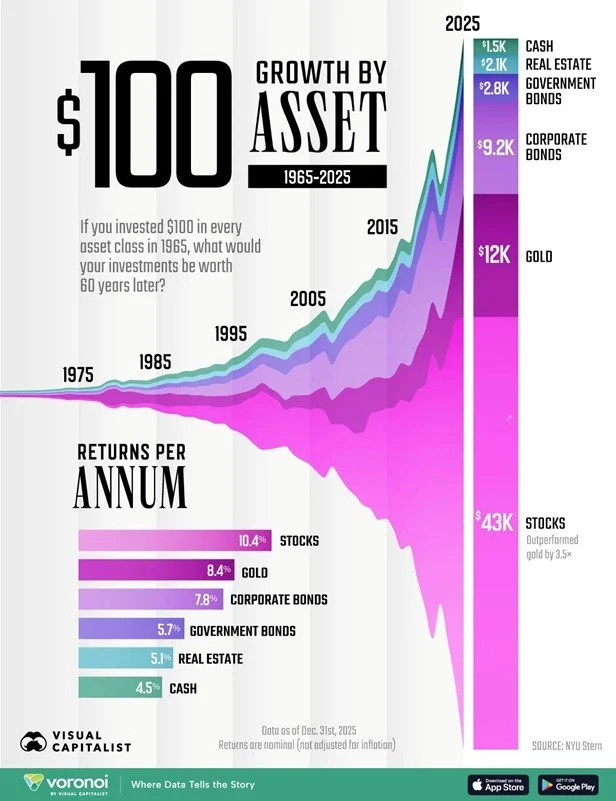

Wisdom in Picture Form

Because by and large, these images speak for themselves:

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Optimism Prism

The media is not a friend of the disciplined and patient investor (especially this month!). Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news.

We present the following as an antidote to the onslaught of negative news:

Drug Potentially Life-Changing for Children with Resistant Form of Epilepsy

This one is a cracker of a story! Although, why replace the historical figures? Can't we have both?

Recommendations

The movie I Swear. Outstanding acting, outstanding directing, and you can see very clearly why it won a host of awards. Quite a difficult watch at times, I'll admit, but gripping from start to finish. You won't regret it.

Keeping a journal. I find writing therapeutic. I always have done, without really knowing why. I was cleaning out a cupboard in our house the other day and I found my journals. I think I have around six of them. I started them in 2011, and it's been an odd habit that I've basically kept up (with large periods of neglect).

I've definitely not been as diligent as the kids since the kids have come along, and the entries have become far more sporadic, but it is incredible to look back on memories that I had 100% forgotten about to read what kind of a person you were at that point in your life.

Strong recommendation from me. The best time to start is today.

That’s us for this month!

All the best,

Andy

The compliance bit:

This newsletter is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.

Past performance is used as a guide only; it is no guarantee of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

The value of investments and any income from them can fall as well as rise. You may not get back the full amount invested.

The Financial Conduct Authority (FCA) does not regulate Trust Advice.

Trusts and will-writing services are not regulated by the Financial Conduct Authority.

Cover will cease on insurance products if premium payments are not maintained.

Generally, pure insurance plans have no cash in value at any time and will cease at the end of the term.