Gifting: To Your Descendants, or HMRC?

Good morning all,

I thought I'd do something light at the start of this, given the current chaos. We will watch and wait but, given the stock market turbulence that will likely follow, I think this reiterates why it is sensible for those in the spending phase of their life to hold a degree of cash, often 2-3 years (not a recommendation and, of course, dictated by your individual circumstances).

Right, after much negotiation and pleading (by me), it is done. The flights are booked, the hotels are sorted, and the WhatsApp group has reached the specific “shambles level” that can only mean one thing: a large group of Scottish people are going to the FIFA World Cup.

Steve Clarke - Sir Steve Clarke, and don't let anyone tell you otherwise - has done something that eight managers before him couldn't. He's taken a squad of players, moulded them into a proper team, and delivered the thing that a generation of Scottish football fans had started to wonder if they'd ever see again.

I have genuinely no idea what happens when we get there. Nobody does. I suspect we'll find out rather quickly. But that, frankly, is beside the point.

Right. Financial planning. Let's get stuck into it.

Opening with the above - a potentially once in a lifetime trip on this occasion - connects to something I find myself saying more and more to clients, particularly those who have done the hard work, saved the assets, and are now sitting on some funds that they have worked decades to accumulate.

Money, at its most fundamental level, is a tool. It is not the goal. It is what enables the goals. The trip. The experience. The time with people you love.

The best financial planning that I am privileged do is not the pension optimisation, the tax efficiency, or specific investment portfolio, although all of those matter enormously. The best financial planning I do is helping people understand what they actually have and giving them the confidence to spend it on what genuinely matters to them.

We are only here once. The people you want to travel with (if that’s your thing) are not going to be around forever. Neither are you, for that matter.

That is not morbid, I hope anyway. That is just honest.

So if there is one message from the above, it is this: the plan, and the money, should serve you. Not the other way around.

On the docket today we have doctors, we have inheritance tax, and somewhere in the middle, hopefully, some genuine value.

Doctor, Doctor — Your Pension Will See You Now

Last Friday morning I found myself sitting in a little side room of the Royal Infirmary of Edinburgh having an unexpectedly frank conversation with two resident doctors (we don’t say ‘junior’ any more) about their retirement planning. The prior Wednesday, I was at a GP practice in the central belt, where three doctors presented me with their NHS pension statements, wearing expressions I can best describe as bewildered.

I don’t blame them.

These are extraordinarily intelligent people. People who make decisions daily that make mine pale into insignificance. And yet they were, every one of them, genuinely confused by their own pension position. That is not a criticism of them. It is a criticism of the system they find themselves in.

The NHS pension scheme is, without question, one of the most valuable employer-sponsored pension arrangements in the country. It is also, without question, one of the most complicated to understand. And the combination of those two things creates a problem.

Doctors, perhaps more so than most of us given the shift pattern, are very busy. Long shifts, significant clinical responsibility, training to attend and/or provide, and more.

A pension statement arrives, it runs to several pages of technical language, and the honest truth is that most of them simply do not have the bandwidth to decode it. They file it, meaning to return to it. And they do not return to it.

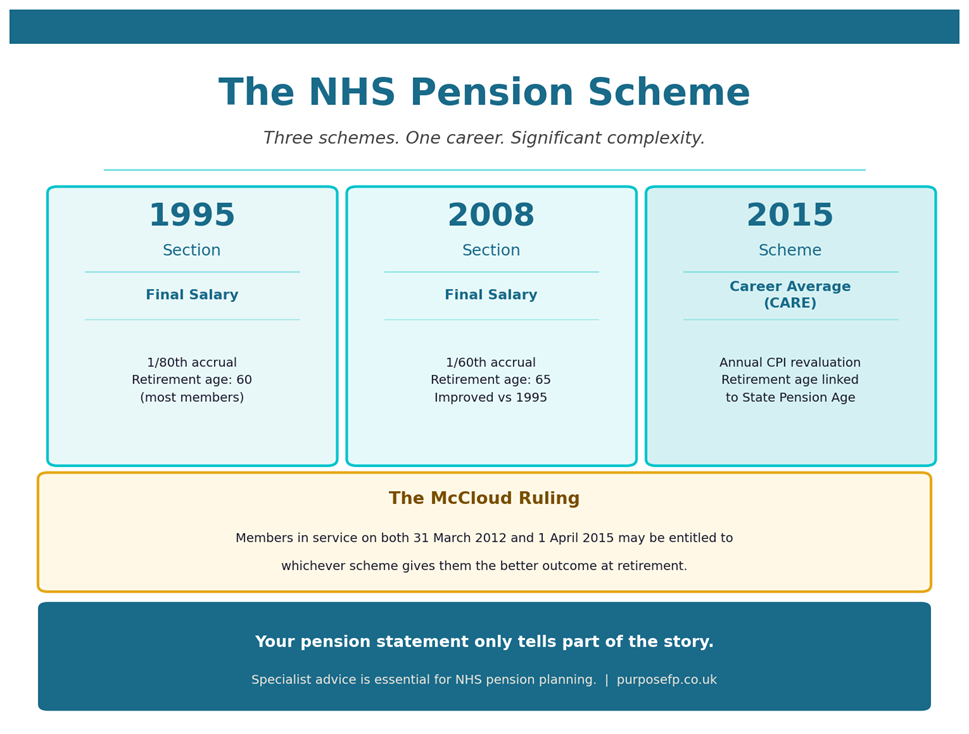

Three Schemes, One Career

Part of the complexity comes from the fact that NHS doctors who have been in service for any length of time may have accrued benefits under not one, but two, (potentially even three!) distinct pension arrangements:

• The 1995 Section — a final salary scheme with 1/80th accrual and, for most members, a normal retirement age of 60.

• The 2008 Section — also final salary, but with 1/60th accrual and a normal retirement age of 65.

• The 2015 Scheme — a career average (CARE) arrangement, where benefits are revalued each year by CPI, and the normal retirement age is linked to the state pension age.

Many NHS doctors have service across all three. The statement they receive attempts to summarise this, but the numbers involved - and the conditions attached (hiya, McCloud!) - are sufficiently varied that even a financially engaged person can struggle to see the full picture.

The McCloud Ruling

Layered on top of this is the McCloud ruling, a legal judgement that found the transitional protections applied when the 2015 Scheme was introduced amounted to unlawful age discrimination. The outcome is that those who were in service on both 31 March 2012 and 1 April 2015 may now be entitled to a "deferred choice underpin" at retirement: the right to choose whichever scheme delivers the better outcome for them.

That sounds helpful. It is, genuinely. But it also means that the value of a doctor's eventual benefit is not fully determinable until retirement - adding another layer of uncertainty to an already complex picture.

Why This Matters

For doctors approaching retirement, or those thinking about reducing their hours, or GP partners considering their practice structure - the decisions made now have significant consequences. Timing of retirement, decisions around additional pension contributions (APCs), and planning around annual allowance tapering all interact in ways that are genuinely difficult to navigate without professional guidance.

The pension statements I saw last Wednesday were not wrong (although I may revisit that in time!). They were just incomplete as a planning tool in isolation. They tell you what you have accrued. They do not tell you when to retire, how to structure the transition, or whether your state pension age and your NHS pension age are going to create a gap you need to plan around.

Fun and games for all concerned. And that’s before one tries to engage with the SPPA; I believe carrier-pigeon is the current mode of communication. And the pigeon is drunk. And starts in Russia.

Giving it Away, Properly: Gifting from Surplus Income

I had an interesting client scenario recently.

A grandparent - comfortably off, investment portfolio well into six figures, income comfortably exceeding their expenditure - had their annual review and naturally, the topic of inheritance tax planning was raised.

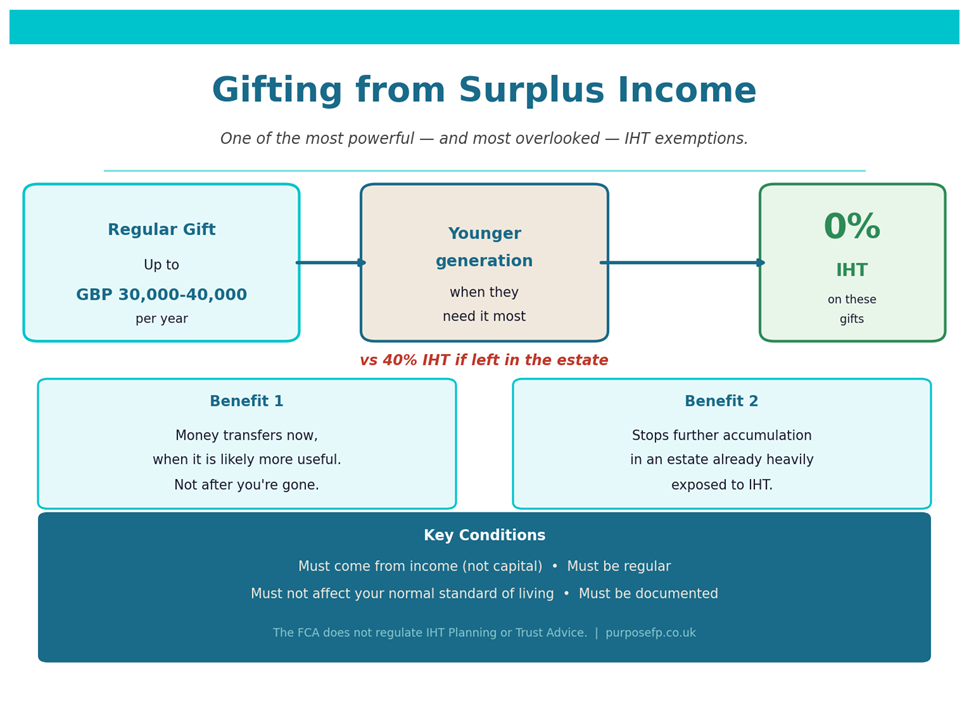

Chatting things through, we found an opportunity. The longer answer involved a restructuring of investment income and a proper look at an inheritance tax exemption that is, in my experience, significantly underused. The exemption in question is the "normal expenditure out of income" exemption, or, as I prefer to call it, gifting from regular surplus income.

Catchy titles, aren’t they? I imagine that if HMRC staff ever formed a band, it would have a name like that. The Exemptions. That’s actually not bad.

What is the Exemption (other than a great name for a band)?

HMRC, in all of their munificence, allow gifts made from your surplus income - that is, income above what you need to maintain your normal standard of living - to be made free of inheritance tax, provided they are regular and habitual. There is no upper annual limit. No seven-year rule to outlive. No diminishing relief. If the conditions are met, the gift is immediately exempt from inheritance tax.

Not too shabby as a starting point, huh?

In this particular case, a careful restructuring of the investment portfolio - shifting from an accumulation-focused approach to a more income-generating one (as capital does not count, interest and dividends do) - combined with documentation of prior unused income capacity, opened the door to gifting well, quite a pretty penny per year, entirely exempt from inheritance tax.

The Dual Benefit

What I find compelling about this route is that the benefit runs in both directions. First, the obvious one: money is reaching the next generation now, in their thirties and forties, when it might fund a mortgage deposit, a business, or simply the financial breathing room that people in that phase of life so often need. Not decades from now, distributed through a probate process, when the grandchildren are in a different stage of life.

But there is a second benefit that is perhaps equally important. This grandparent's estate was already significantly exposed to inheritance tax. The portfolio was continuing to grow and, whilst this is obviously not a bad thing, compounding further into the 40% zone. Every additional pound of investment return was, in effect, being split 60/40 with HMRC. By restructuring to facilitate regular gifting, that accumulation stops. The estate is, deliberately being reduced, or perhaps “capped” is the better word there.

It's not foolproof, of course. The investments could still experience some capital growth, but again, hey, it’s better to have 60% of something than 100% of nothing.

The Conditions Matter

This exemption is powerful, but it is not available without proper documentation. HMRC will want to see that gifts were made from income rather than capital; that they were regular and intended to be habitual; and that they did not affect the donor's normal standard of living. The form to be aware of is HMRC's IHT403, which executors may need to complete on death. If the paperwork is not in order, the gifting history can be challenged.

The practical advice is to document everything contemporaneously - 26 Scrabble points, but for the boffins amongst you this is a moot point, you’d never lay it in a single play - ideally a simple annual summary showing income received, normal expenditure, and gifts made. It’s not onerous, and fair enough in the grand scheme of the exemption available.

Simply because this exemption is likely to work in this instance, please note that it may not work in any other instances. Seek individual advice.

The FCA does not regulate inheritance tax planning or trust advice. Levels and bases of, and reliefs from, taxation are subject to change. Every estate is different — advice should be tailored to individual circumstances.

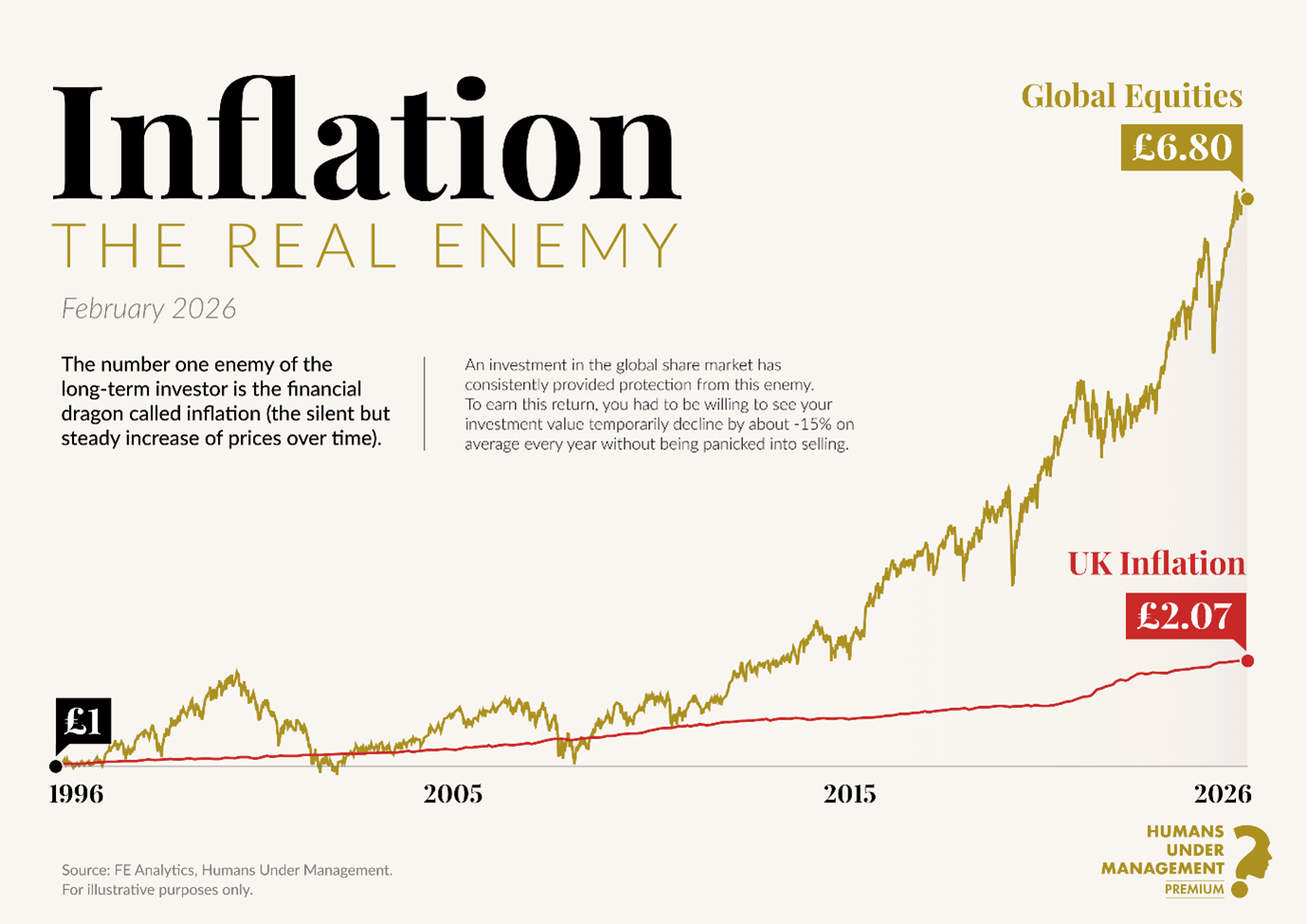

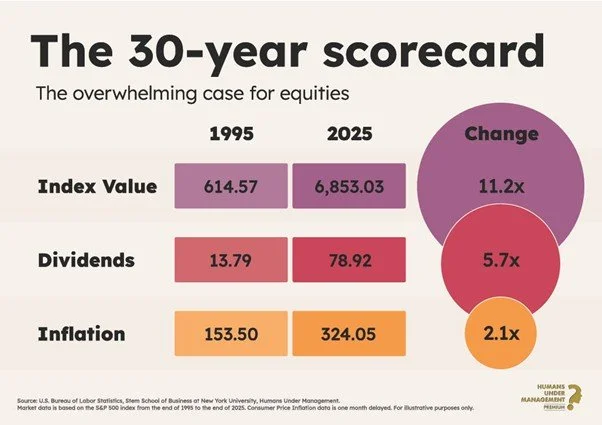

Wisdom in Picture Form

Because by and large, these images speak for themselves:

Optimism Prism

The media is not a friend of the disciplined and patient investor. Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news.

We present the following as an antidote to the onslaught of negative news:

Recommendations

• Wispr Flow: a very cool voice-to-text dictation tool that genuinely seems to work (unlike many of the others I have tried!)

Amazon Luna — this one is for the frustrated ex-gamers among you (yes, I am one). You know who you are. The people who used to have a console, then got a mortgage and a family and a dog and have not switched it on in three years.

That last part is a lie. I’ve started playing Kingdom Come: Deliverance II and already lost a few hours (days, weeks?) to it.

Anyway, Luna is Amazon's cloud gaming service, essentially Netflix for video games. What a time to be alive.

That's us for this month!

All the best,

Andy

The compliance bit:

• This newsletter is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.

• Past performance is used as a guide only; it is no guarantee of future performance.

• Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

• The value of investments and any income from them can fall as well as rise. You may not get back the full amount invested.

• The Financial Conduct Authority (FCA) does not regulate Inheritance Tax Planning or Trust Advice.

• Levels and bases of, and reliefs from, taxation are subject to change and their value will depend upon personal circumstances. Taxation and pension legislation may change in the future.