Daylight Robbery via The Commons

Good morning all,

I’ve bought my son his first ever set of “figures”. A strange word, figures, for what are basically dolls for young boys, but you know, Marvel ones. Can’t wait to see his little face light up when he gets them. I’ve bought them for his 5th birthday, and he’s currently 3. That gives me a solid 13/14 months of nostalgia before I – begrudgingly - hand them over.

Although, when I was wee, I think it was Teenage Mutant Ninja Turtles and the legendary Action Man, and not Ironman, Thor, and the like.

Flailing around desperately here, wondering how I can bundle this into a financial planning reference. I bought the figures second hand; something about being frugal, saveth-the-pennies-maketh-the-pound, sort of thing? That won’t work. Action Man, and how with his solid financial plan he was able to sail off into the sunset for a well-earned retirement? Also poor. Let's give up and move on.

Some good content this month (the opening paragraphs aside), even if I say so myself. We’ll take a look at the difference between the markets and the economy, I’ll have a stab at some financial journalism, and we’ll do a quick overview of things here at Purpose FP Towers.

Oh yeah, and we also “lost” our first client. But for a very lovely reason, and likely only a temporary basis. A nice story all the same.

Here we go.

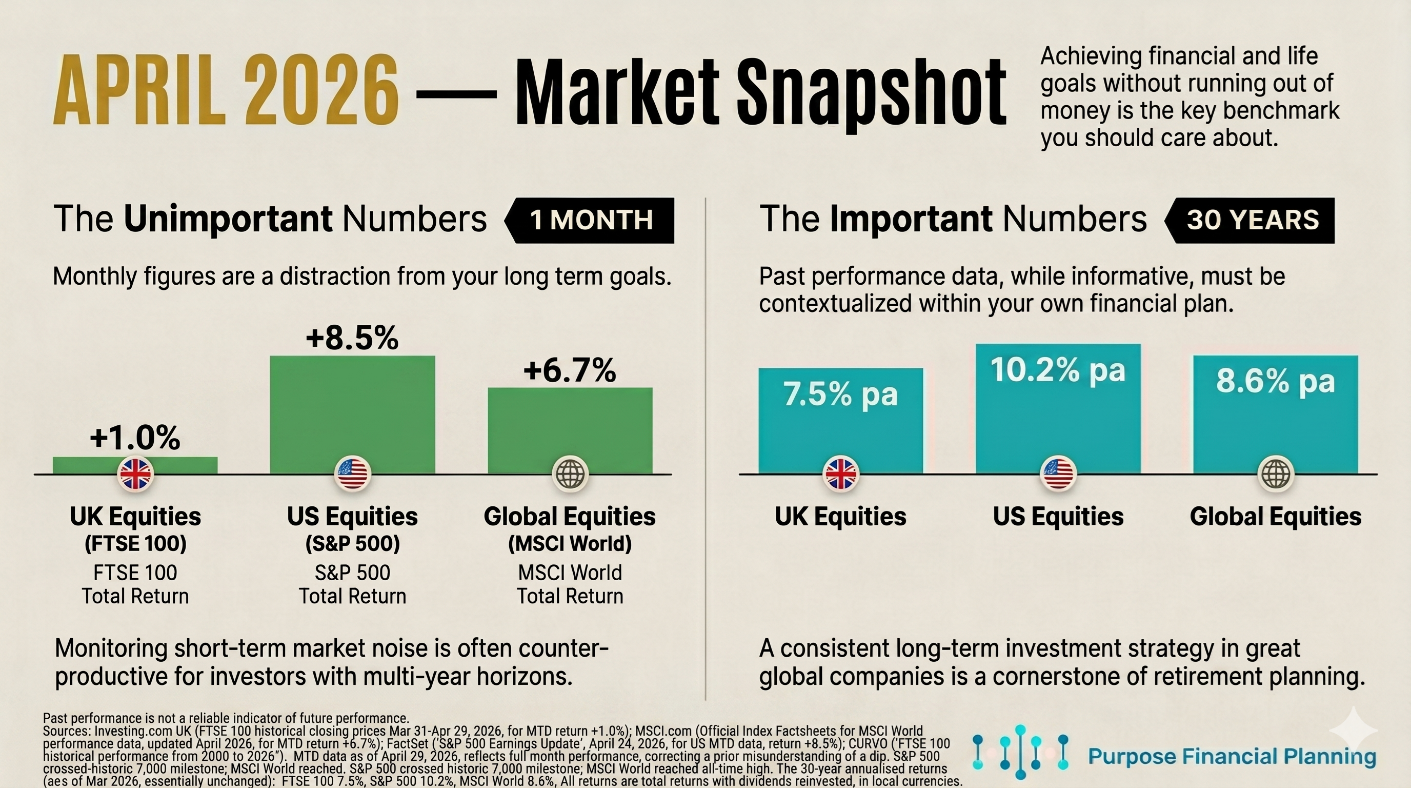

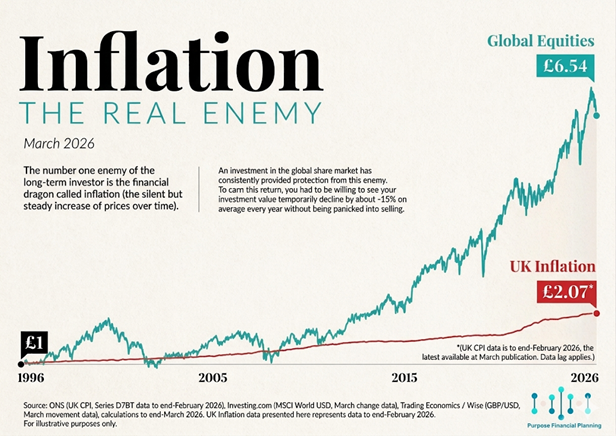

Monthly Market Visuals

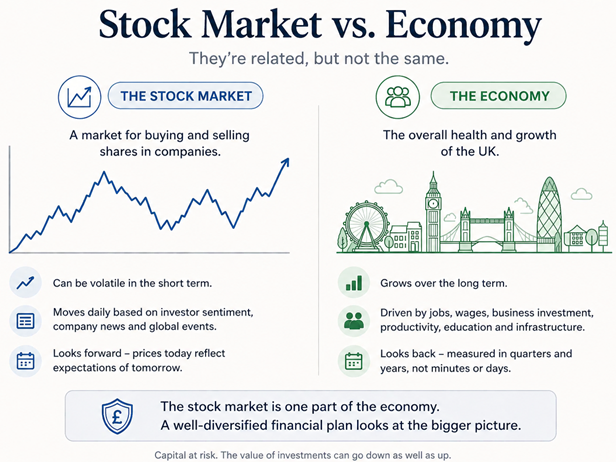

The Markets & The Economy

I was listening to Times Radio, as is my wont in the morning, when something caught my ear a little more than usual.

They brought on an investment commentator to explain the seemingly illogical situation of the stock markets – particularly the US one – continuing to go upwards despite all of the current geopolitical tensions. This was mainly focused around the Iran War and impending inflationary fears, driven largely by the increase in the oil price.

Understandably, Stig and Kate McCann (the Times Radio presenters) were confused as to the deviation between the upwards direction of the stock market and the general negative consensus around macroeconomics.

This is something I see a lot. It’s often something that new clients and I will spend some time discussing, as, through no fault of their own, new clients or new investors often arrive into the office with preconceived ideas and concerns about what impact ‘ABC global event’ will have on the stock market, and therefore, their financial situation.

And sure, sometimes, there are apparent connections between an economy of a nation and it’s stock market. If people don’t have any disposable income, for example, it is naturally going to squeeze the revenue of hospitality companies and discretionary spend companies in that particular nation.

But far more often than not, quite the opposite is true. Any given nation can be in the apparent depths of economic despair, whereas the stock market will march upwards happily, uninterested in the latest employment or inflationary figures. There are a few reasons for this, which I thought it might be helpful to touch on:

1) Companies, or equities as they are often known in investment parlance, are one of the few proper defences against the ravishing effect of inflation. This is because a company has the all-important ability to set its own prices. If their supply costs go up (which they cannot control, largely), it is only logical for said company to increase the cost of the good or service that they provide. For if they do not, their profit margin will decrease, and the company will be poorer as a result.

Individuals, broadly, cannot do this – certainly not to the same extent. We cannot simply send HR an email saying we have decided to increase our wage by 10% to cope with the increased cost of living. Thanks-very-much-cheers.

So even if a given nation is suffering from quite significant inflation, a company has a natural defence against this often not available to other participants in the economy.

2) Regardless of what is going on, there is generally always a way to make money from it. In current times, the oil companies are doing just grand. In Covid, the technology companies saw their share price skyrocket, despite global economic discretionary spend plummeting. In war times, weapons manufacturers benefit, and so on.

3) The third reason, and there are a few more, is more of a logical one. The economic health of a nation is largely a backwards-looking exercise. Inflation is driven by what has happened over the previous 12 months, employment data is similar.

Markets, by contrast, are often forward-looking. Share prices today are often based on a company’s potential future revenues, as well as their revenues of today.

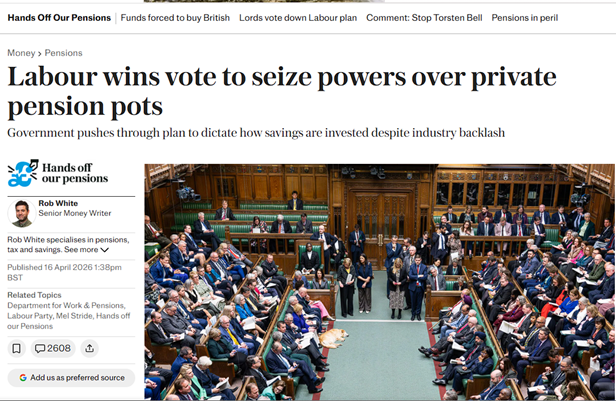

Attempted Daylight Robbery

Now, this is a good news insert. It is, honestly, although it may not read like that at times. And that is for one reason, in that I was a tad furious (an oxymoron?) with the actions of the UK Govt. I’m honestly surprised that this wasn’t front page news across all of the papers, although admittedly, the opaque nature of the following topic could make it prohibitive, although it in no way lessens its importance.

Anyway, let’s set the scene.

Back in May 2025, 17 of the largest UK pension providers signed the “Mansion House Accord”. Now, that was a mistake, but given the recommendations were entirely voluntary at this point, who really cares, right? The upshot was that the Govt was trying to “encourage” (watch this space) pension schemes to invest in UK private markets. This was with the feel-good mantra that they were “backing British business” and of course, the Govt hoped that by bringing this shiny new pension cash into the UK economy, they could force stimulate UK growth, something which moves about as fast as I would wadding through treacle. With dishwashers strapped to my legs.

The problem for the UK Govt was that investors just aren’t all that keen on the UK right now. They’re especially not keen on UK private equity, where it is becoming harder for these companies to raise finance than it would have been 20 or 30 years ago.

Last year, 88 companies either delisted or transferred their primary listing away from the London Stock Exchange - the most since 2009.

Now, there are a couple of reasons for this, in my view. Chiefly among them is a complete misunderstanding of the concept of investment risk, with our largest pension schemes often encouraged by UK regulators into Liability-Driven Investment strategies (don’t ask) in place of the much simpler equity market.

Over the past 25 years, UK pension funds have reduced their allocation to equities from 73% to 27% - and they have slashed their allocation to UK equities from 53% to just 6%.

In the linked article, I particularly like the following line:

“To be fair, pension funds and insurers have not so much lost their risk appetite as had it kicked it out of them over the past few decades by the cumulative impact of well-intended reforms to accounting standards, regulation, and tax. At every turn, they have responded rationally to the incentives and disincentives in front of them. It is also important to stress that there is no silver bullet to reverse course, and that much of the pensions money that has been sucked out of the UK equity market is not coming back.”

So, that was the Govt’s problem to solve. And rather than, you know, genuine reform of tax and regulation to encourage a pro-business environment (and the growth/jobs/tax revenue that would no doubt come with such reforms), or an evolution of the concept of risk in investment markets (although, to be fair, we do seem to be making progress there), they decided more radical action was required.

Enter, the aforementioned Mansion House Accord. And what became a voluntary feature of the reforms was soon to become mandatory.

Over the past few weeks and months, and with a disappointing lack of mainstream media coverage, the UK Govt, led by Work and Pensions Secretary Pat McFadden, attempted to force UK workplace pension schemes – and ladies and gentlemen, there is a lot of mullah in their coffers. £1.1 trillion in DB schemes, £650 billion in DC workplace, and £415 in the local government pension scheme – to invest at least 10% (!) of their assets in private markets, with half of that going into UK private markets.

As you might have guessed, I am strongly opposed to the idea that the Govt should be able to mandate your pensions savings – this is your money, for your retirement – to plug a rather noticeable gap in inward investment into UK private markets. The UK public markets we could discuss, but the private markets, which are generally awash with high-fees, over-inflated valuations, and a complete lack of transparency, is, frankly, outrageous.

A pension exists for one primary purpose – to support the individual in their retirement. It does not and should not be a plaything for the Govt – of any colour – with which to attempt to plug gaps in the economy.

Here we get to the good news. On the evening of 27 April, the Lords rejected the bill for a third time, with a motion brought by Lib Dem peer Baroness Bowles passing by 197 votes. The next evening a revised, watered-down version passed through the Lords. It’s not perfect, with mandating still a possibility - the government have to produce a formal report examining the barriers to UK private market investment prior to using their powers – but it’s a lot better than where we started.

Still, something for you all to keep an eye on.

For clarity, the above generally applies to workplace defined contribution pensions. In other words, that's most modern-day workplace pensions. Not advice to anyone, but perhaps another reason to consider the independence of a private pension, free from such intrusions.

Pension decisions should be based on individual circumstances and advice. Nothing in this newsletter should be construed as individual advice.

Business Update

I used to do these periodic updates on the business, but have been a little lax lately. Let's correct that now!

I am currently fortunate enough to look after the affairs of 58 fantastic families. This ranges from young people earlier in their wealth growing journey, to those with very complex affairs, and everything in between. Thank you all for your trust and your confidence.

Actually, I recently parted ways with a client. But it was the very definition of a great relationship having come to an end, and perhaps not even that.

One of the first clients to join the firm was someone who had some spare capital following the sale of their Edinburgh home, and they needed some advice around tax-efficient investment. Fast forward to now, we are some £80k to the good (the vast bulk of which has been entirely tax-free), with the sum being gifted to a family member as part of a property purchase.

A very good end all round:

(Shared with permission).

With annual review period in the rear-view mirror, I now have space to work with new clients. Therefore, if you know of anyone who would benefit from a chat around any element of their personal finances, please do forward my details to them. I do not intend for the firm to grow much more in terms of client numbers, but there is some space available.

I’d be delighted to have a conversation.

Please note that the above example is client-specific and should not be considered typical or guaranteed.

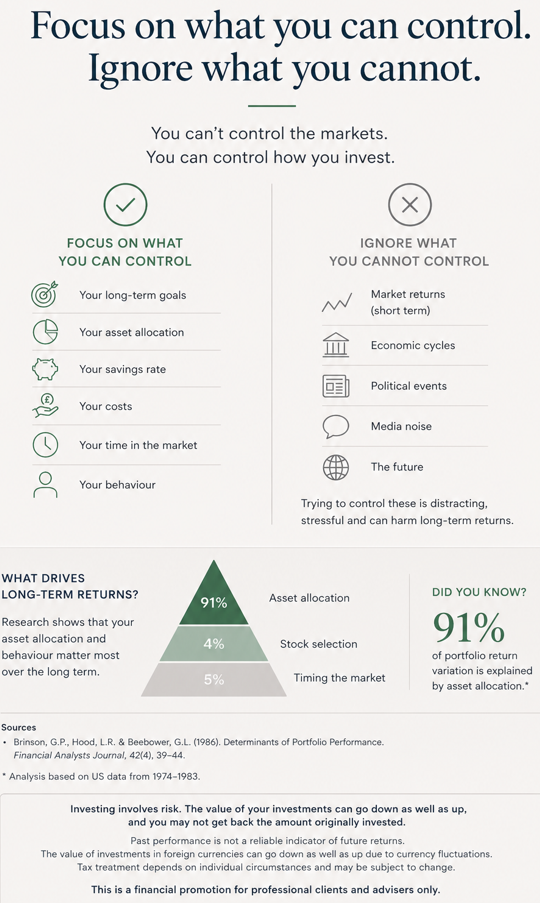

Wisdom in Picture Form

Optimism Prism

The media is not a friend of the disciplined and patient investor. Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news. We present the following as an antidote to the onslaught of negative news:

- A six-year-old girl has her sight restored by gene therapy at Great Ormond Street

- Renewables now meeting all new global electricity demand

- And of course, Artemis II.

Recommendations

1. House of Guinness on Netflix. Really enjoyed this, from Stephen Knight, creator of Peaky Blinders. Found it acting generally superb and the characters were extremely engaging in their own unique ways. Delighted to see there'll be a new series in due course.

2: Keeping the Guinness theme going, Guinness Zero! I'm fond of an alcohol-free beer when I'm out and about, and Guinness Zero on draft is a whole new ball game. Cards on the table, I actually sent it back as I thought they'd inadvertently brought me the real thing. Wonderful stuff. Lucky Saint for the lager version.

3. Acquired Podcast - This one's been on my radar for a while, and I finally gave it a proper go this month. Hosts Ben Gilbert and David Rosenthal do exhaustive, multi-hour deep-dives into the histories of remarkable companies - from Hermès to Nike, Berkshire Hathaway, and the Bank of America. It's part business history, part investment analysis, and entirely addictive.

That's us for this month.

All the best,

Andy