June Already!

Good morning all,

The frequency of which I am watching these highlights is not quite at “cause for concern” levels, but the numbers are definitely creeping up. It’s that iconic radio commentary when Tierney’s goal goes in, and then the sheer euphoria for Mclean's. If you’re in a rush when you’re reading this, but you want a wee pick-me-up, give yourself a treat and simply forward on to the 4:20 mark. Don’t say I’m not good to you.

In our WhatsApp group, the camp seems a little split regarding the renewal of Stevie Clark's contract before the World Cup has even started yet. In today’s opinion-piece-that-you-haven’t-asked-for, my take on it is he should absolutely have been given the contract extension. Sure, lessons need to be learned from the shambolic showing at Euro 2024, but we can only really go up from there.

And on that note, a small public service announcement. I’ll be in the states from the 12th June until the 26th. Tickets for all three games, thank the gods, and it’s shaping up to be the trip of a lifetime. Emails will be checked daily, work will be done v.sporadically (honesty is the best policy), but please take this as fair warning that your email may start to twiddle its thumbs in my inbox, wondering where my reply is. It’ll get there, but a little later than usual.

Okay, there we are then, Let’s get back to the good stuff.

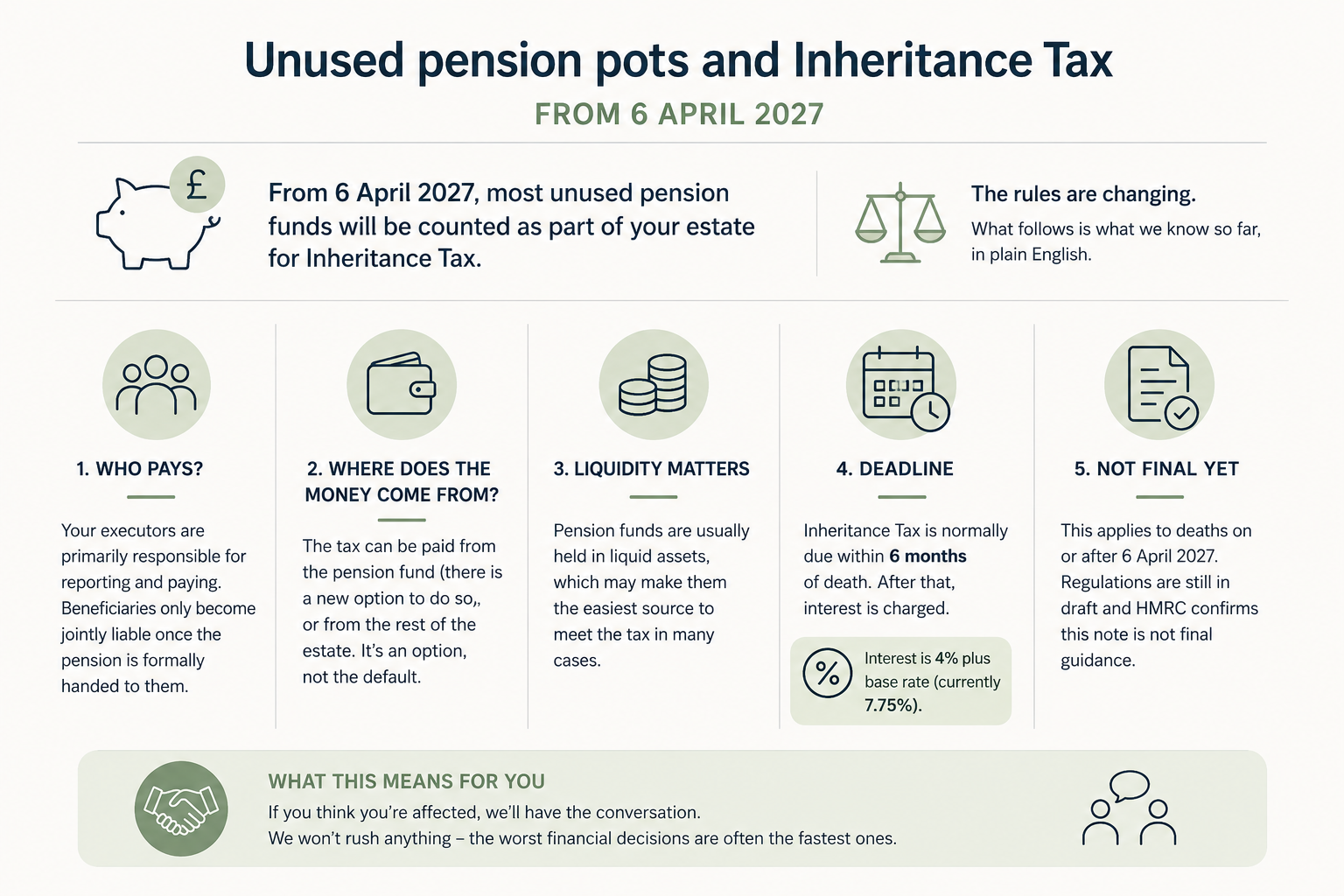

Pensions & Inheritance Tax – How It Will Work

We’ve had some much-needed clarity re the implementations of inheritance tax on unused personal pension pots from the 6th of April 2027. It's not particularly good news, but let’s unpack it all the same.

Wish as we might, it doesn’t seem to be going away.

HMRC published its technical note on inheritance tax and pensions in May, and the financial corner of the internet promptly did what it always does in reducing eighty-odd pages of legislation into a handful of bullet points, some of which are right and some of which are mince. So let me have a go at telling you what it actually says, in plain English, before you read something weird and wonderful on social media.

The headline is this. From 6 April 2027, most unused pension funds will be counted as part of your estate for inheritance tax. Many of you know this well, and indeed, for some of you, we have started to look at alternative IHT options.

For years, your pension was the one corner of your wealth the taxman couldn't get his hands on at death. Many have said that this led people to stop treating pensions as a pure retirement savings vehicle and started treating it as the most tax-efficient way to pass money down the line. Perhaps so, but those were the rules of the game.

The Treasury however, have taken notice. You can argue about the wisdom of it - and plenty are - but I’ll try and stick to the planning angles here.

A few things worth getting straight, first of all.

Who pays? Not your family directly, despite what you'll read. Your executors are primarily on the hook for reporting and paying; beneficiaries only become jointly liable once the pension is formally handed to them.

Where does the money come from? You'll see "paid from the pension fund" quite often. It can be, there's a new scheme that allows it, but it's an option, not the default. The tax can equally come from the rest of the estate.

That said, for any of the firm’s clients, almost always the pension fund will be in quite liquid (easily converted to cold hard cash) assets, compared to other assets in the estate like property, art, etc - although this will depend on the individual scheme and investments.

So, it may actually be easier to use the pension in many cases. Anyway.

The deadline is six months from death. That's the normal inheritance tax deadline, and whilst it's nothing exotic, can feel particularly harsh in practice. Thereafter, interest starts to accrue. Quite hefty interest it is as well; it is now 4% plus base, so, at the time of writing, that is 7.75%. If the estate's liability is sizable, that could be quite painful.

As you know and stating the obvious, none of this is formally in play yet. It applies to deaths on or after 6 April 2027, the regulations are still in draft, and HMRC itself stresses the note isn't the final guidance.

If you think you're affected, rest assured, that's a conversation we shall be having. What we won’t do is rush anything - the worst financial decisions are often the fastest ones.

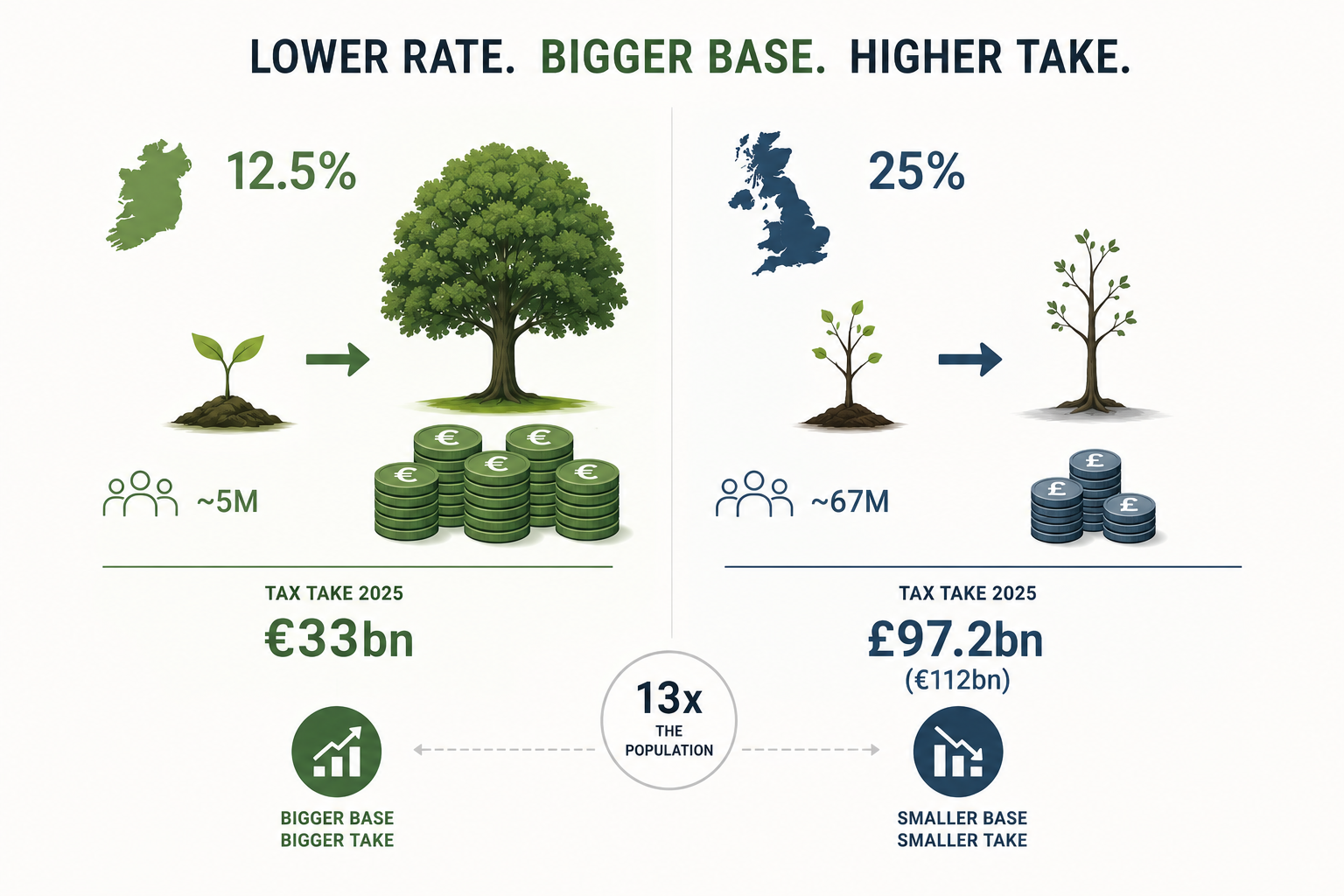

A Low Tax Rate That Raises A Fortune

The difference between tax rate and tax take is something that, in my humble option, we could perhaps debate a little better in the UK. My starting assumption is that most people want the country to raise more money, which can in turn be used to improve public services, roads, etc.

The Laffer curve is now getting a lot of air time, and this section is on a similar theme.

In 2025, Ireland, a stone’s throw away and made up of around five million people, collected around €33 billion in corporation tax. There’s your starter figure, and it was up roughly 17% on the previous year.

The Irish headline rate, however, is a mere 12.5%. For comparison, the UK charges a corporation tax rate of 25%, and has approximately 13 times the population of Ireland.

Now, this is a gross over-simplification, but run with me for a second. If we simply took the €33 bn that Ireland raised and multiplied it by the multiple of population of the UK, this would give us €429 billion of UK corporation tax receipts. However, in the same period that Ireland raised €33 bn, the UK, with its vastly higher rate and roughly thirteen times the population, raised only £97.2 bn (€112.17bn).

Sit with that for a moment, because it cuts against almost everything we instinctively believe about tax. We tend to assume that if you want more revenue, you raise the rate. Higher percentage, bigger take. Simple. Except it very often isn't, and Ireland is probably the clearest illustration in Europe as to why.

There are two ways to grow a tax. We can grow the rate, or we can grow the base from which the tax comes. The rate is the percentage charged, and this is the big noisy event in the media. Different parties have different ideological views on which way that rate should go, but, in my opinion, this doesn't necessarily lead to more money in the coffers for the Treasury.

The base is the pile of profit you charge it on. Raise the rate and, all else being equal, you collect more on the same pile. But all else is rarely, if ever, equal. Push the rate high enough and you start to shrink the very pile you're taxing, as activity slows, moves, or simply never arrives. You can end up with a bigger slice of a smaller cake, and increased discontent alongside, as the nation leans more and more on a smaller pool of productive individuals/companies/etc.

Ireland – and others, but let’s focus on them for now - went the other way. It kept the rate deliberately, famously low, and used it to grow the base instead. Decades of a stable, low, predictable rate persuaded a remarkable concentration of multinationals to book real activity there. The pile of taxable profit grew enormously, and 12.5% of an enormous pile turned out to be a great deal more than 25% of a modest one. The low rate wasn't revenue forgone. It was the bait that built the base, and the base expanded at a rate of knots.

Now, the Irish model is not a free lunch and I'm not pretending it is. Those receipts are heavily concentrated in a handful of very large firms, which makes them fragile if the global winds change. The Irish themselves are rightly cautious about spending the windfall as though it'll last forever, and now operate a healthy budget surplus- can you imagine?

There's also the small matter of the new 15% global minimum rate, which is only now coming into force and reshaping the whole picture. So, it's not a perfect template.

But still, the underlying lesson holds. The rate and the base are not the same, and we could perhaps consider some new ways of thinking in the UK. A lower rate on a thriving base can comfortably beat a punishing rate on a base that's quietly packing its bags.

This is a simplified comparison for illustration only. Corporation tax receipts can be affected by many factors.

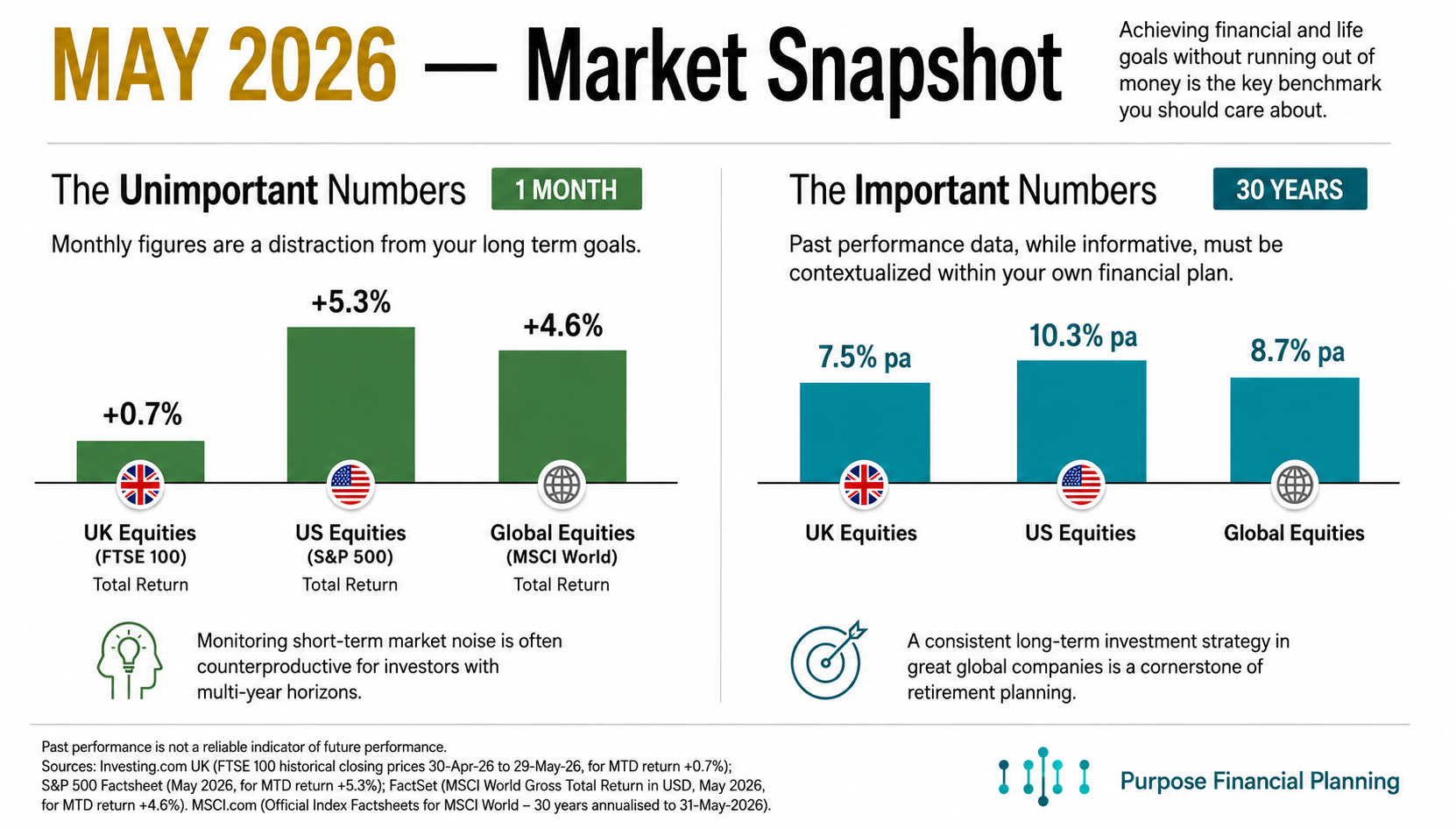

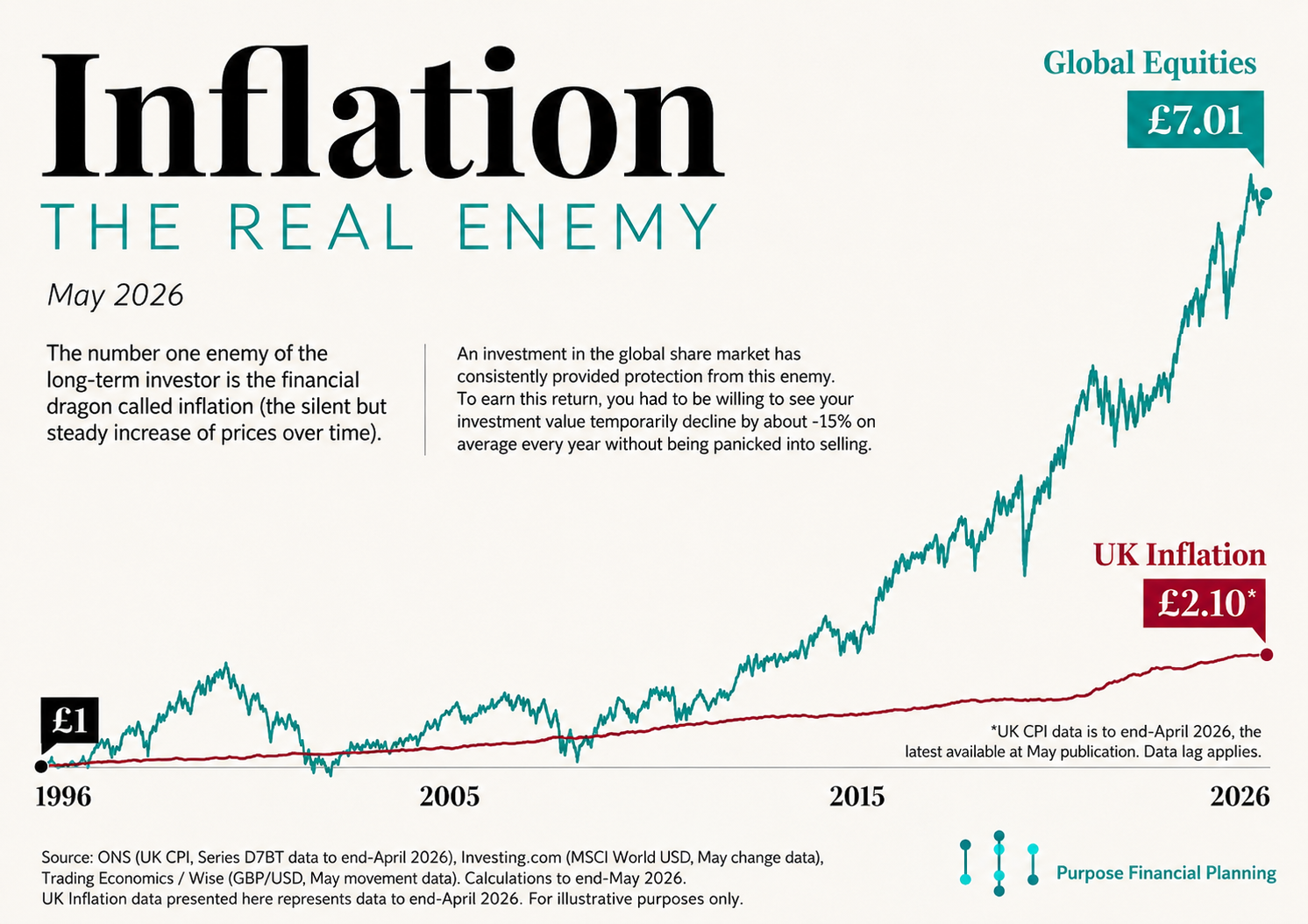

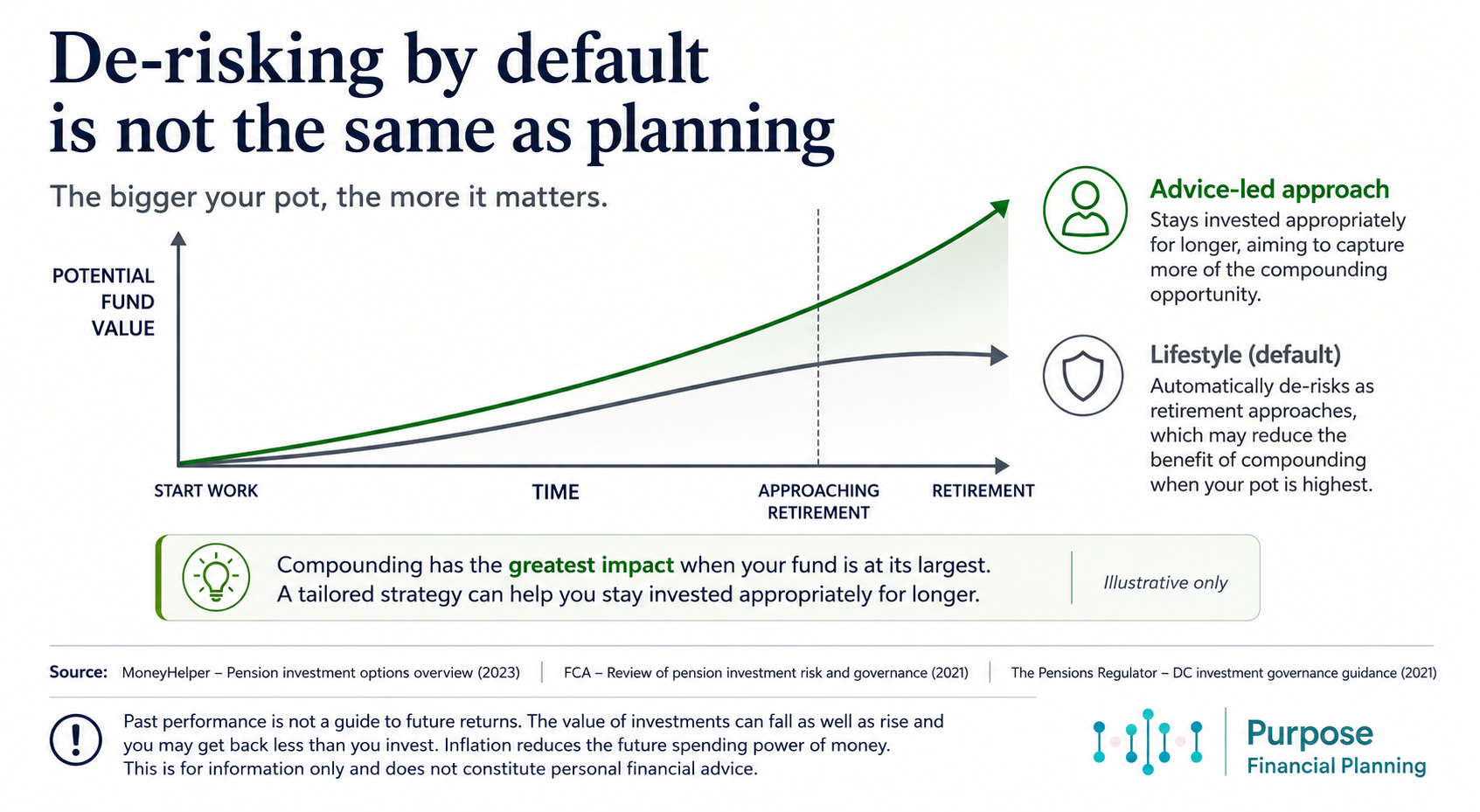

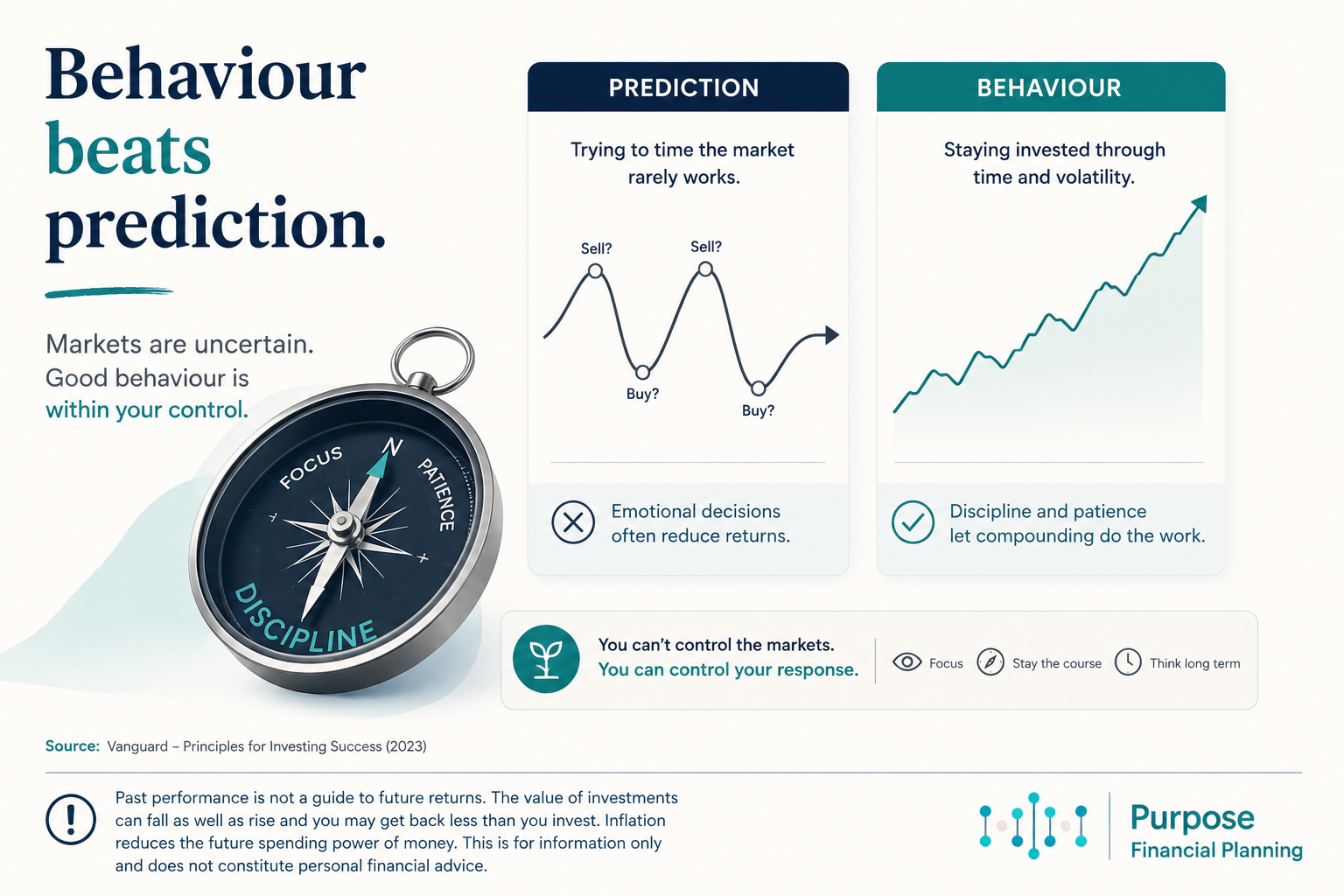

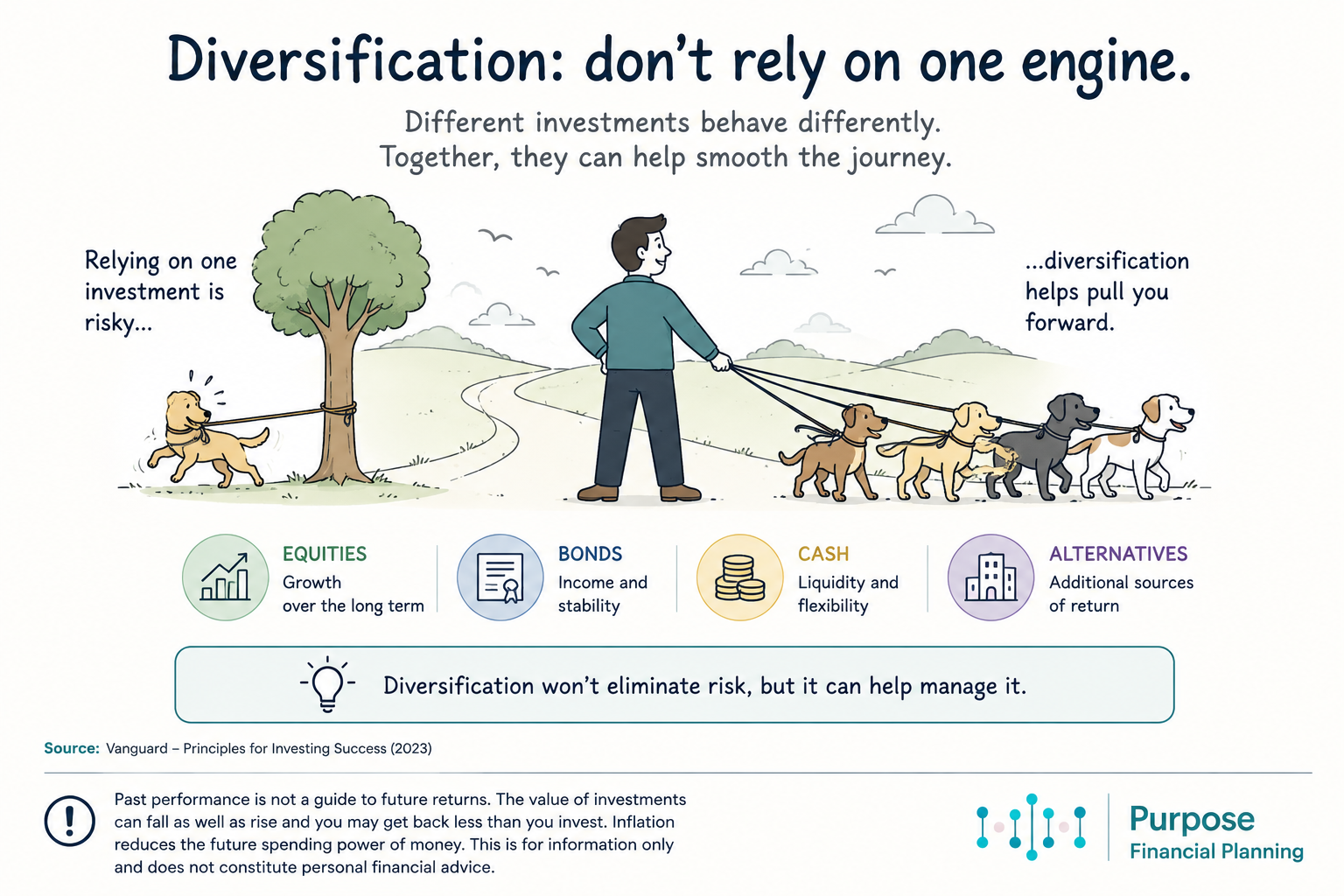

Wisdom In Picture Form

Because, as ever, these images tend to speak for themselves:

Images is purely for illustrative purposes, and the right approach will depend on individual circumstances.

Optimism Prism

The media is not a friend of the disciplined and patient investor. Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news. We present the following as an antidote to the onslaught of negative news:

- African countries that were first to roll out the RTS,S vaccine have reported a significant reduction in child deaths, according to a landmark report this month.

- ‘Groundbreaking’ bowel cancer trial reports no relapses

- The benefits of coffee (I have a vested interest in this)

Recommendations

Seatfrog. I found myself down in London last month. Decided to upgrade and using this app is a nice way to do it. Much cheaper than going directly and a vast improvement to the overall journey. Thumbs up.

A mammoth three and a half hour recording on the origins of the investment behemoth Vanguard and the wonderful Jack Bogle, to whom we all owe a big debt. If you're looking for a deep dive or something to entertain you over a series of dog walks, it's worth a go. Definitely one for the geeks though (I am now so cool, I have Vanguard socks. 2 pairs! Worth the conference trip alone).

I recently found myself driving from Midlothian down to the borders, and what a drive it was. I went down to Galashiels, and that is a seriously under-rated part of the country. Get yourselves there and explore.

And a wee Brucie-bonus, in honour of Sir Stevie Clarke.

That’s us for this month!

All the best,

Andy

The compliance bit:

This newsletter is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.

Past performance is used as a guide only; it is no guarantee of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

The value of investments and any income from them can fall as well as rise. You may not get back the full amount invested.

The Financial Conduct Authority (FCA) does not regulate Trust Advice.

Trusts and will-writing services are not regulated by the Financial Conduct Authority.

Cover will cease on insurance products if premium payments are not maintained.

Generally, pure insurance plans have no cash in value at any time and will cease at the end of the term.