Boatloads of Cash

Good morning all,

What an experience that was.

A tremendous time in the States, and it flew by very quickly. Much like Scotland’s participation in the actual tournament, there we are. We didn’t deserve to qualify, and that’s life supporting Scotland.

It's always good fun until the football starts.

What was remarkable however was the fun, the laughs, the memories. Outstanding in every department. Some of you will have seen the coverage of the Tartan Army, particularly in Boston, which seems to have dominated my social media feed for some time.

The strangest moment for me personally however was standing in line at Disney, trying to entertain the wee ones whilst battling the heat ourselves, and a very nice American guy in front started talking to us. I think this was just after the first game.

He was giving us hints and tips for that particular park (there are 7 of them I think) and chatting away about this and that.

Side note, did you know that a Florida resident gets unlimited annual use of all Disney parks – plus parking, which isn’t cheap at $35 per day – for only $65 a month? Absolute bargain.

The nice chap then proceeded to ask me about the shops here, and “how have you found the supermarkets?” He mentioned this, he says, as he has been following a “random Scottish guy” who was making his way around their classic shops like Walmart and Target whilst filming the experience. He brought his phone forward to show me the video of my brother that Fraser had put together a few days before.

You can’t stuff like that up – superb.

I’ll write a little more about my US experience in a while, but for right now, let’s get into the usual format.

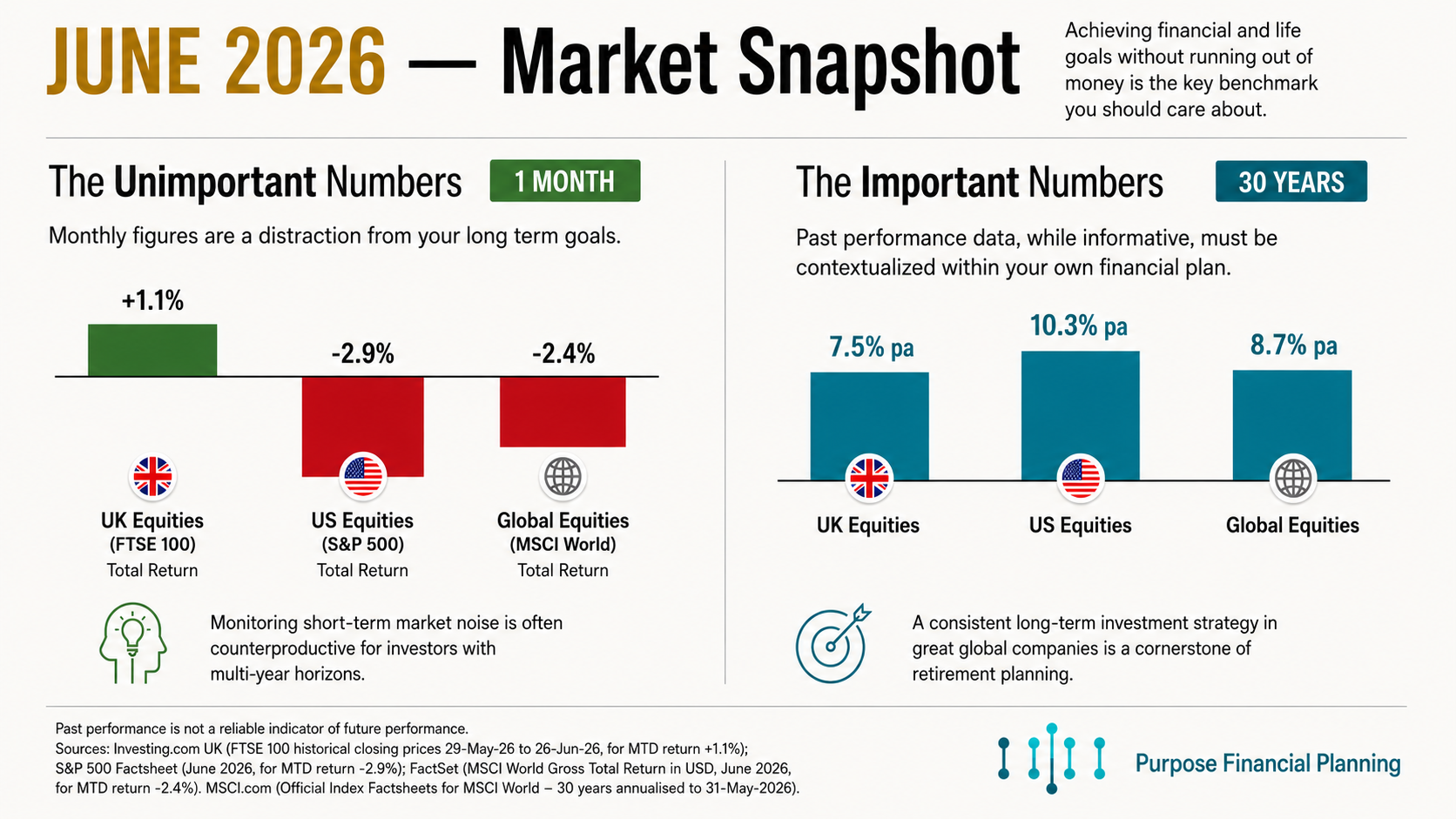

Monthly Market Visuals

Companies Sitting On Truckloads of Cash

Conducting meetings with clients, I spend a decent chunk of our meeting gently explaining why holding too much cash is a quiet disaster over the long-term - inflation nibbling away at the real value, year after year, the whole cheery routine. But then, have a nosy at what some of the world’s biggest companies are doing:

In other words, Warren Buffett is sitting on roughly $382 billion in cash. So why can he do it, Mr adviser, and I can't/shouldn’t?

It's a fair question, and a good one. Let's get our teeth into it.

That $382 billion is no ordinary sum. It's the largest cash position in Berkshire Hathaway's history, and it's more than Microsoft, Alphabet and Amazon are holding put together. Berkshire is the clear outlier, but it's far from alone. A recent piece from Visual Capitalist ranked the fifty companies holding the most cash on their balance sheets, and the piles are eye-watering across the board. Interestingly, thirteen of the top fifty are financial firms - banks and insurers - which matters, and we'll come back to it.

So why do companies hoard the stuff?

The least glamorous reason is also the most important: they need it to run. Wages, suppliers, tax bills, keeping the lights on. Money coming in and going out is rarely as smooth as a spreadsheet suggests, and a business that runs out of cash at the wrong moment is a business in trouble, however profitable it looks on paper. Cash is the oil in the engine.

Then there's the buffer. A cushion for when things go wrong - a recession, a shock, a global pandemic that shuts the world for the guts of two years. The companies that sailed through 2020 in reasonable shape were, by and large, the ones with money in the bank. Nobody ever regretted a rainy-day fund when it actually started raining.

The third reason is the interesting one, and it's where we get to the interesting bit. Cash is optionality. It's the ability to act decisively when everyone else is losing their heads. Buffett's most famous line is to be "greedy when others are fearful", but being greedy requires having something to be greedy with. He holds cash precisely so that when markets fall and good businesses go on sale, he can stride in and buy while others are forced sellers. To be fair, it’s worked for him thus far.

Two more things worth a mention. First, cash is no longer dead money. For years interest rates sat near zero and holding cash earned you a fat nothing. Today, with rates higher, that same cash earns a respectable return parked in short-term government debt. Alphabet alone has earned billions in interest income in recent years just by sitting on its hoard. Second, those thirteen financial firms aren't really "choosing" to hold cash in the way Apple is. Banks and insurers are required by regulation to hold large liquid buffers, so their cash means something rather different. So, treat their inclusion with a pinch of salt.

Right. That's the corporate picture. Now, why should any of this matter to you?

Here's the first reason, and it's a pleasant one. If you own a global index fund, or a pension, or an ISA invested in the world's great companies - and most of you likely do - then you already own little slices of Berkshire, Apple, Microsoft and the rest. Those cash piles are, in a roundabout sense, partly yours. It has never been easier to own the best businesses on earth, run by some of the sharpest people on earth, and to let their discipline quietly work on your behalf.

But the more useful point is the mirror this holds up to your own finances.

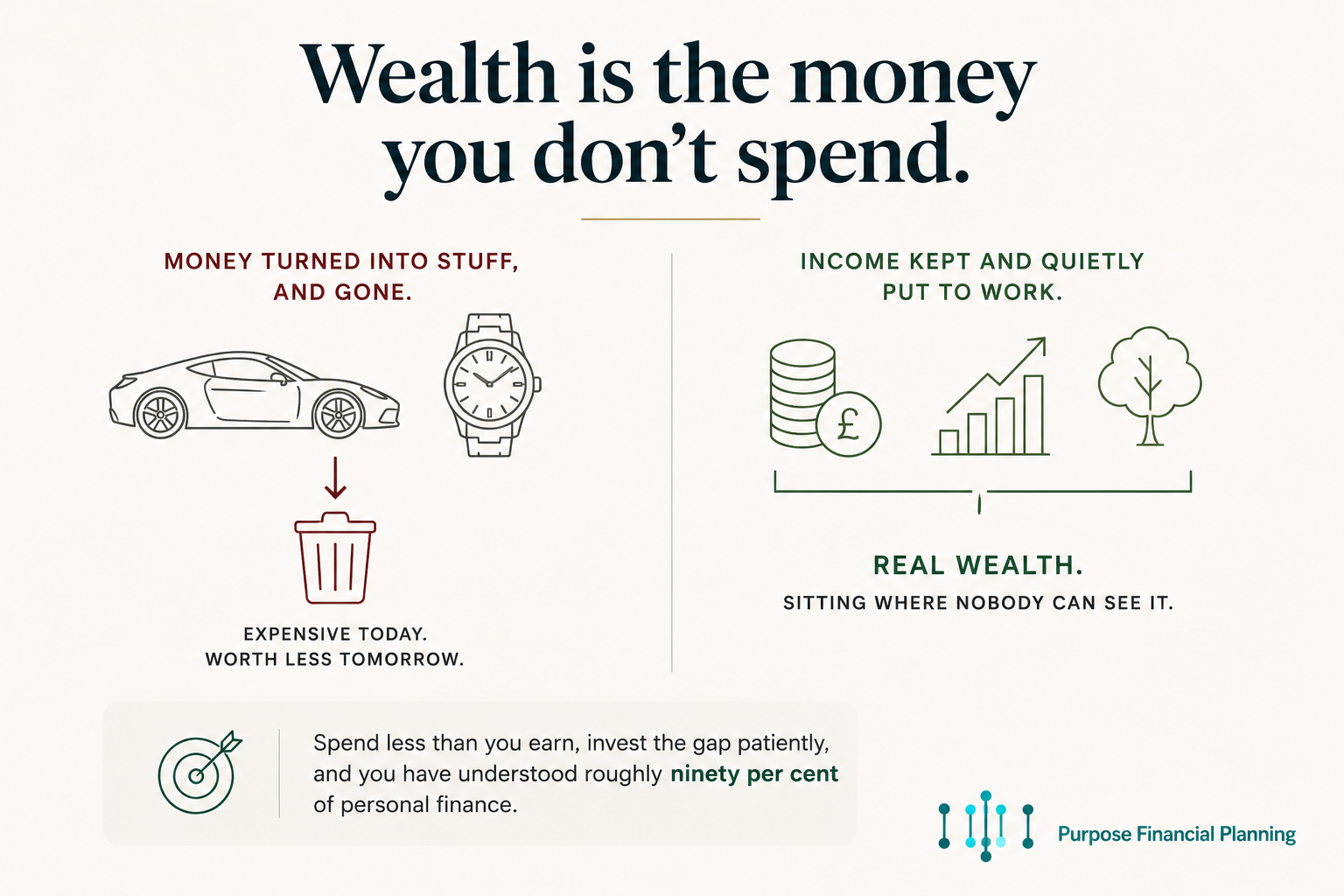

Companies hold cash for three reasons: to run the day to day, to weather the bad times, and to pounce on opportunity. The first two apply to you almost exactly. Your version is the emergency fund - three to six months of outgoings, kept liquid and boring, for the broken boiler or the unexpected redundancy. That cash you absolutely should hold. It is the working capital of a household, and going without it is how a small problem becomes a large one.

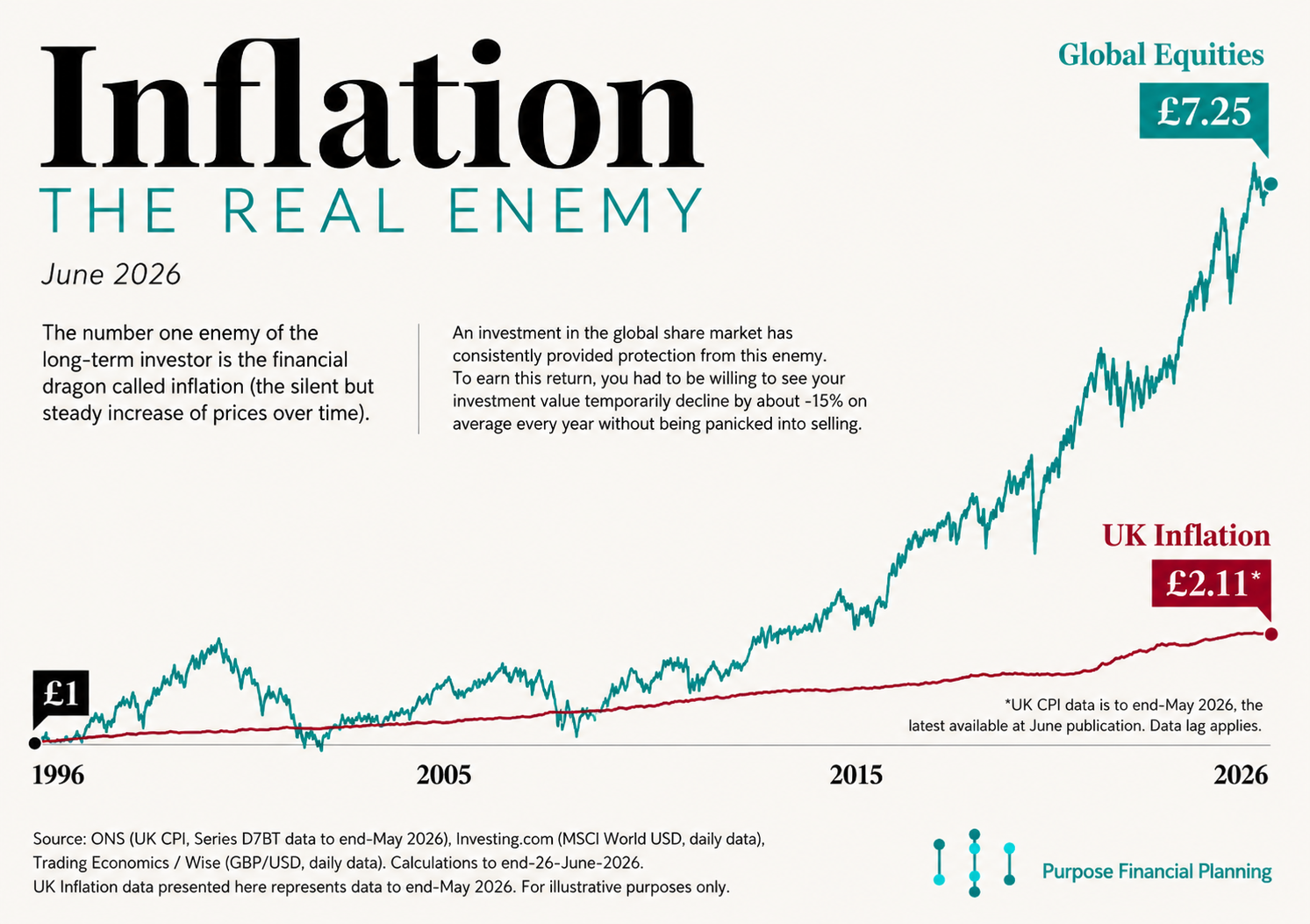

The trouble starts beyond that buffer, and it's here the comparison breaks down in a way that matters. When Berkshire holds cash, it earns a tidy rate and stands ready to buy a railway. When you hold a great heap of spare cash in a current account earning next to nothing, it simply sits there being quietly eroded by inflation. (Regular readers will know my views on inflation, the real enemy of the long-term saver. I'll spare you the rerun.)

And then there's the optionality trap, which catches more people than any other. Companies hold cash so they can act. A great many individuals hold cash so they can wait - for the right moment, for things to "settle down", for the perfect entry point that somehow never quite arrives. We've covered the futility of timing the market before, so I won't labour it, but that distinction is the whole game.

The contrast is this. A company sitting on a cash pile is usually making a deliberate, considered decision. An individual sitting on years of salary in a savings account "just in case" is, more often than not, quietly avoiding one.

Hold enough cash for emergencies and for spending you can see coming, and perhaps a buffer on top. Make sure whatever you do hold is at least earning a fair rate rather than mouldering away. And whatever you do, don't think cash is the answer long-term. Inflation is the silent destructor of wealth.

The door, as always, is open if you'd like to talk it through.

Purpose Financial Planning Turns Three

…and I have loved the “journey”, a word that seems to be in vogue these days.

I won’t make this a long entry, as you are all busy people, so I will simply say thank you. Thank you first and foremost to the clients of the firm, without whom this would all be a silly dream. To those that have referred business, to those that have offered advice, kind words, or listening ear.

Thank you all, and here’s to the next three years.

Observations from the States

Now, this is all mostly anecdotal, but I thought it'd be useful to jot down some quick observations from my two and a half weeks state side.

I think in the UK and across many European countries, we have this impression of the USA in general as being somewhat of an unstable place. An environment, perhaps, where people are looking over their shoulder, worried about how the next healthcare bill will leave them financially, worried about their national politics, etc.

What I saw was very different, and might not be natural reading for some.

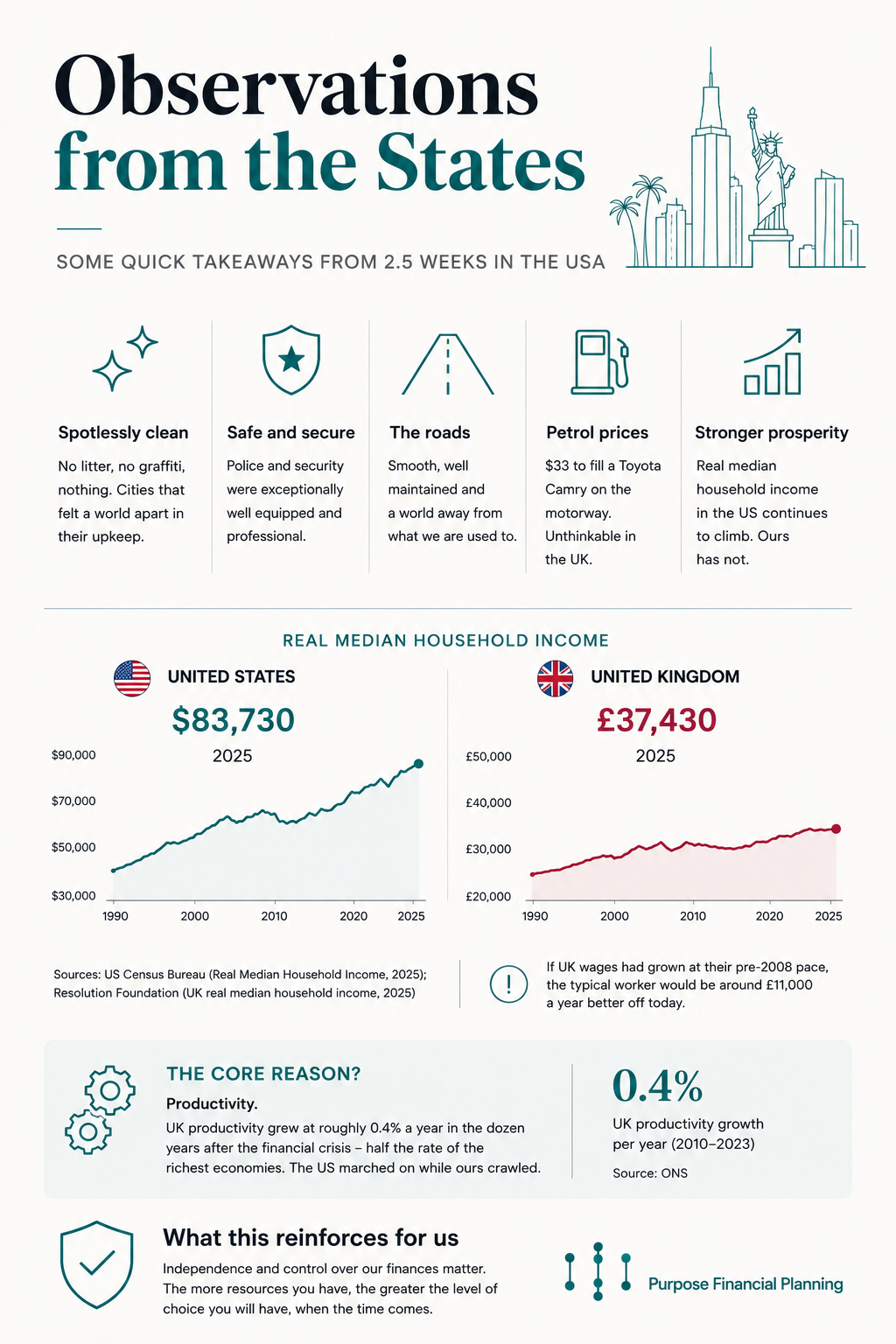

Firstly, it was clean. Not just clean, spotlessly clean. No litter, no graffiti, nothing. Fair enough. We were primarily in tourist places, and you would expect them to be clean, but is Edinburgh, Glasgow, or London? I wouldn't say so, not to the same extent. Boston, Miami and even New York were like cities from completely different realms by comparison.

On returning to Edinburgh airport, we were greeted by a massive puddle in the floor of the baggage area, covered up with sodden newspaper and cardboard. I don’t think the Americans would have tolerated that at one of their major airports. Not the best first impression for international arrivals.

The size of things. I guess that’s nothing new. But one thing that was very notable was how well equipped the police and security were there. Again, perhaps we saw very specific units set out alongside the major events that we went to. Even looking at the cars, the American police are driving supercars compared to what the UK police are. The level and professionalism of the private security around the Disney Parks; leagues away from anything you would expect to see at any UK tourist attraction.

The roads. We would have had to drive intentionally looking for a pothole, such were the quality. It’s a little different in the UK, and let’s just leave it there.

Petrol. Again, no surprises here, but it cost us a mere $33 dollars to fill up a Toyota Camry ON THE ACTUAL MOTORWAY (the “turnpike”, I believe was the local lingo), using one of the big companies with the red and yellow signs. You’d be taking out a second mortgage if you did that frequently in the UK.

So, I came home asking the obvious question. Was that just holiday goggles, or is there a point here?

The data suggests it’s worth a look. Real median household income in the United States hit $83,730 last year, and it has kept climbing through the 2010s and beyond. Ours has not. The Resolution Foundation reckons that if British wages had carried on growing at their pre-2008 pace, the typical worker would be around £11,000 a year better off than they are. We have had the best part of two decades of going nowhere, whereas the USA has excelled.

I mean, for example, look at the wages on offer here working with one of their car wash chains:

Yes, Buc-ees might be an outlier, and yes there is more to it; healthcare, the welfare state, the tax system and more, but it’s an interesting discussion all the same.

The general impression I was left with was that they are leagues in front of us.

I am not trying to talk down the UK, and there is plenty the USA gets badly wrong that we get right. But the gap in everyday prosperity is real, and most of it traces back to one unglamorous word: productivity.

Ours grew at roughly 0.4% a year in the dozen years after the financial crisis, half the rate of the richest economies. By comparison the states was 1.3% (US Bureau of Labor Statistics / FRED), which may not seem like a big difference year on year, but over 13 years that adds up significantly.

No vast lessons or wisdom in this piece, simply my observations. Others will have very different opinions, I am sure.

Tying it into the work that we do for our clients, I would simply say that my observations have reinforced the importance of independence and control over our finances, rather than relying on the state. The more resource you have, the greater the level of choice you will have, when the time comes.

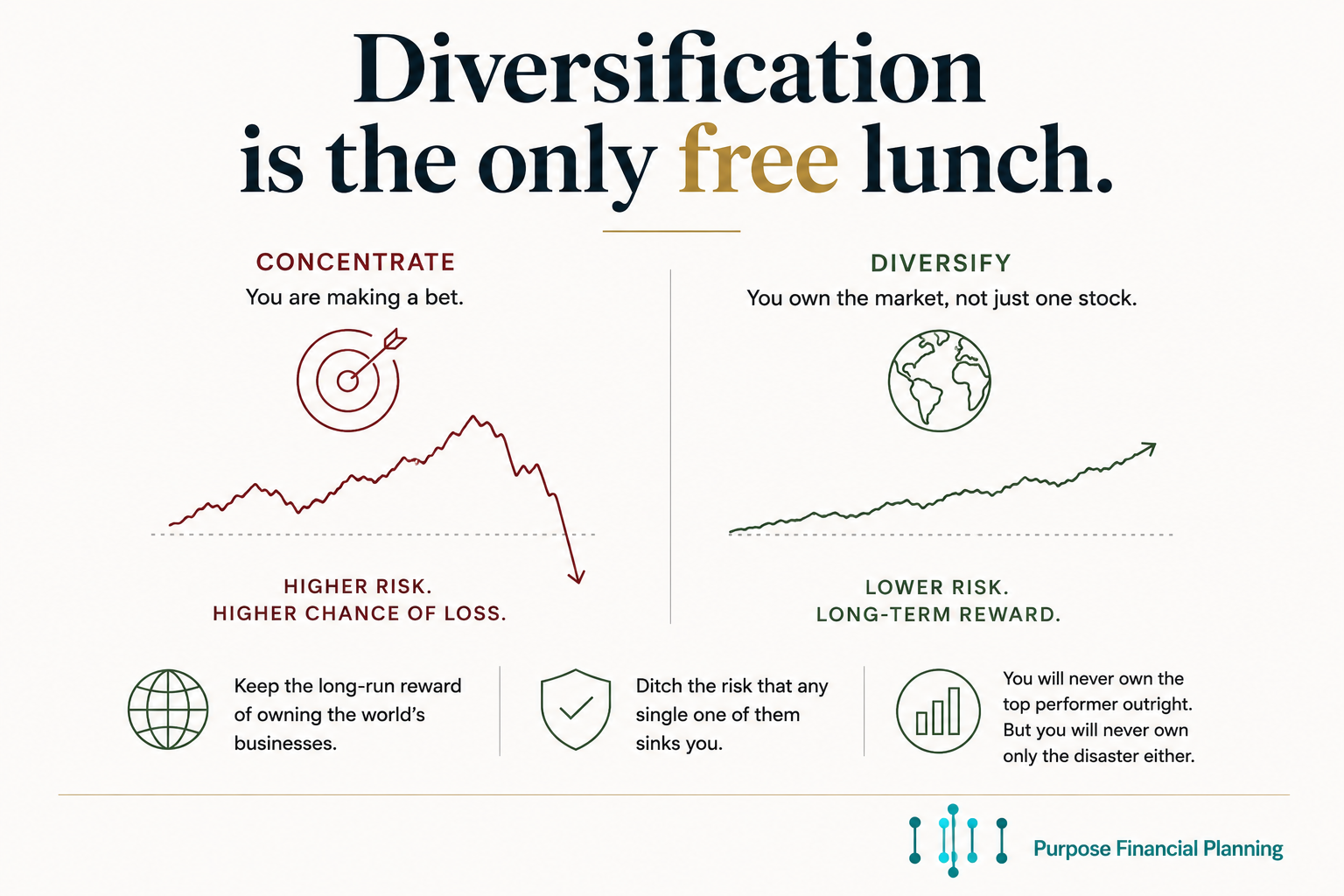

Wisdom in Picture Form

Optimism Prism

The media is not a friend of the disciplined and patient investor. Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news.

We present the following as an antidote to the onslaught of negative news:

‘Skomer's puffins have their best year on record

Two million electric cars, and the line that bends

Recommendations

1. Virgin Atlantic.

We flew with them to and from the states and the whole way there we had complimentary Starlink Wi-Fi. It saved our bacon as well, as I had to call the accommodation to verify something before we landed. A strange experience doing it over WhatsApp from 10,000 ft in the air.

2: Disney. Just do it. It’s awesome, embrace it. If my 4-year-old can go on the Tower of Terror – dragging his nervous Dad alongside him – then so can you. They actually have this Star Wars experience ride where you are captured by the First Order and Kylo Ren chases you – great fun.

3. Boston – A smashing city, and well worth a visit. Nice people. Just say you visited with the Tartan Army and you’ll probably get the red-carpet treatment.

That’s us for this month!

All the best,

Andy

The compliance bit:

This newsletter is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.

Past performance is used as a guide only; it is no guarantee of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

The value of investments and any income from them can fall as well as rise. You may not get back the full amount invested.

The Financial Conduct Authority (FCA) does not regulate Trust Advice.

Trusts and will-writing services are not regulated by the Financial Conduct Authority.

Cover will cease on insurance products if premium payments are not maintained.

Generally, pure insurance plans have no cash in value at any time and will cease at the end of the term.