Pensions, ChatGPT, and Inspector Rebus

Good morning all,

Storm Floris can’t make its mind up, as I type this on a ‘5-minutes of sun followed by 5-minutes of cloud and rain sort of day’. Midlothian is just on the cusp of the amber weather warning, but so far, it’s not bad. I tend to judge my weather by Mac’s desire to go outside. If he’s insistent he’s not leaving, a bad day of weather it is.

Naturally, having now had this newsletter “signed off” by compliance a few days after writing, it is now lovely outside and the above intro doesn’t really make sense. Never mind.

I start these newsletters with a list of topics, deciding which ones to include that month. Sometimes it is a bit sparse and there’s not a lot going on. Today however, there is lots to write about, and alas, some topics will have to be left out. One such being my concern/impassioned plea/rant that the UK financial services sector has done far more harm than good with its mischaracterisation of “risk” when describing investment.

However, that newsletter will likely land me in IFAjail (compulsory reading of the FCA Handbook 15 times a day, with barred windows made of 3D Excel spreadsheets), and I don’t fancy that right now.

Monthly Market Visuals

Inheritance Tax on Pensions – UK Govt Feedback

The UK Government published its response to the inheritance tax (IHT) on pensions consultation on the 21st of July 2025

Let’s address the headline stuff first - they are sticking to their guns. IHT on pensions will apply from 6th April 2027.

They are also sticking to the rules around double-taxation on pensions post age 75. This part of the change I consider far less thought-through (there’s an obvious joke there about the Govt thinking through any of its decisions, but I’ll leave you to formulate that as you desire), as it creates the potential for some very nasty tax consequences indeed.

For example:

· Individual dies post 75 with an estate in excess of the IHT thresholds.

· IHT of 40% is due on the value of the pension. Ouch.

· Income tax on any funds the beneficiary draws down (ranging from 0% - 48% on the net value). Very ouch.

· The pension value taking the individual’s estate above £2m, leading to them losing some of their IHT nil rate band (namely the residential nil rate band worth up to £175,000). See below.

So, there we are.

The good news is that the pension scheme administrators are not going to be solely responsible for paying the IHT due on pensions from the value of the pension. The liability can be aggregated with the value of the estate and paid from assets elsewhere. So, more work for the personal representatives and lawyers, but the pension scheme administrators are happy.

That one was a move of common sense, thankfully. A direct consequence of the various pension providers responding to the consultation, so well done to all of them:

“In light of the consultation responses, the government has decided not to proceed with this proposed model. Instead, PRs — who are already responsible for administering the rest of the estate — will be liable for reporting and paying Inheritance Tax on any unused pension funds and death benefits from 6 April 2027.”

We have also had some positive news with the government clarifying that pension death-in-service benefits will not be liable to IHT. This ensures consistency, especially for benefits from schemes like NHS pensions, which would otherwise have been caught under earlier proposals.

Ongoing dependant’s pensions paid under scheme rules (e.g. defined benefit/final salary pensions to surviving spouse or child) are also excluded from IHT, thank goodness.

But that was about the long and short of it. The main tax consequences are still very much there.

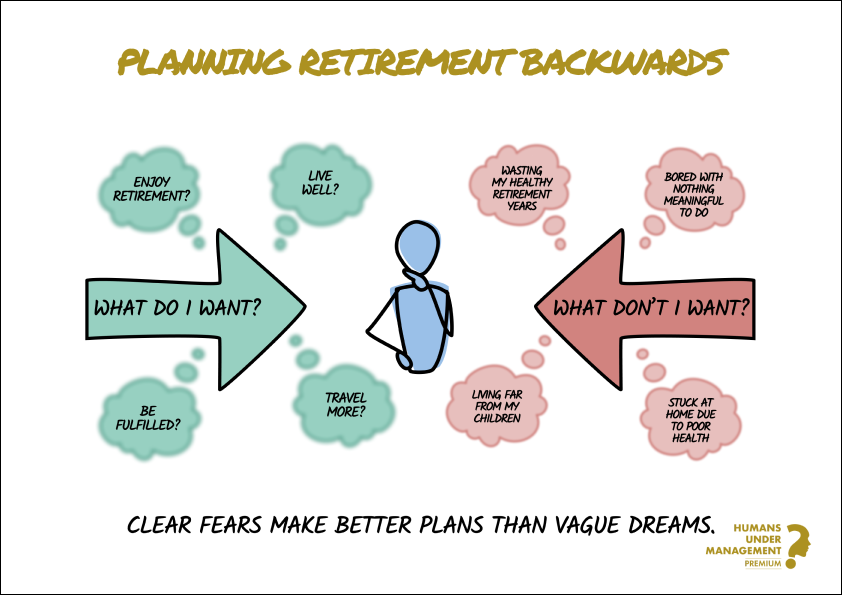

Thinking Backwards: A Different Way to Plan Your Retirement

Most people plan their retirement by looking forward, trying to envision their perfect future. “What do I want to do? Where do you want to live?” Unfortunately, most people have no idea what they want.

Ask someone to describe their ideal retirement and you'll get vague answers. "Travel more." "Spend time with family." These sound nice, but they're not specific enough for planning.

An alternative approach that may generate better answers faster: start with what you don't want. This comes from Charlie Munger, who made "invert, always invert" one of his core principles. Instead of asking "How do I succeed?" consider asking "How do I fail?" and then work to avoid those outcomes.

When you ask, "What would make my retirement miserable?" the answers come quickly. These fears are specific and actionable. Avoiding them brings you remarkably close to the life you want.

The financial regrets of retirement get all the attention. Not saving enough, retiring too early, and underestimating costs are common financial pitfalls.

There are however other things that are just as important as money:

Missing your active window.

Most people have roughly 15 years of healthy, mobile retirement before things get harder. Yet many waste these precious years because they didn't plan for travel and adventure while they could still enjoy them.

As I often tell clients, spend more in the early years whilst you are able to enjoy the travel. This is very much part of the plan.

Losing your identity and purpose.

After 40 years of career structure, it is natural to feel a bit lost. A new retiree may have money, but does it lack a sense of usefulness or meaning? The days could feel empty if work provided more than just income.

Relationship isolation.

Some retirees find themselves living far from adult children and grandchildren, or they've let friendships fade during busy career years. Money can't buy back lost time with people you love.

Neglecting health in your 50s and 60s.

This is when prevention matters most. Poor health choices during these years can significantly reduce the quality of your entire retirement, regardless of how much money you have saved.

Take care of yourself, so that you can in turn can take care of others.

Inversion Thinking & Retirement Planning

While most people do post-mortems after something goes wrong, a “pre-mortem” imagines failure before it happens. It's simpler than it sounds.

Begin by imagining you're 80 years old, reflecting on your retirement with profound regret. Ask yourself: “What went wrong?”.

What do you wish you'd done differently? Don't overthink this. Your gut reactions are usually the most telling.

Next, get specific. Instead of "I wish I'd travelled more," ask "Where exactly did I want to go, and when was the best time to do it?" Instead of "I should have stayed healthier," ask "What specific health habits would have made the biggest difference?"

Then work backwards to today. For each regret, identify what you need to start doing now to prevent it. If your biggest fear is losing touch with your children, consider where you'll live in retirement. If you're worried about losing your sense of purpose, consider developing interests beyond work.

The goal isn't to solve everything today; it's about gaining clarity on what matters to you, so you can begin incorporating those elements into your life. It may help when you look back on things.

Your Next Step

Most retirement advice focuses on the numbers. How much to save, when to retire, how to invest. These are important, but they're not enough.

The retirement that will bring you fulfilment requires thinking beyond the spreadsheet. It requires imagining not just the money you'll have, but the life you'll live with it.

Inversion thinking gives you a practical way to do this. The pre-mortem exercise we described isn't a one-time activity. Your fears and priorities will change as you get closer to retirement. What feels important at 50 might look different at 60. Regular check-ins help you stay on track.

The financial piece of retirement is well understood. Do the work now to avoid the lifestyle regrets later.

Tell Us Once

I may have mentioned this previously, but it bears repeating as it is a very good resource.

Dealing with the loss of a loved one is hard enough without navigating layers of paperwork. One service that many families aren’t aware of - but can make a difficult time just a little bit easier - is Tell Us Once.

This government-run service lets you report a death just once, and they’ll automatically notify several departments and organisations for you; things like HMRC, the Department for Work and Pensions, the DVLA, and your local council. Unfortunately, the private institutions you still have to do yourself, but it’s a good start.

It’s free to use and in my experience, it can save families hours of phone calls and form filling. When I guide clients through estate planning or act as a sounding board after a bereavement, I often highlight practical steps like this to ease the burden and give families more time to focus on what matters most.

Whilst writing on this topic, I would also share a free resource that I threw together a few years ago. It’s a list of everything an individual may have and where important things like passwords and wills are stored. I hope it’s helpful.

For some reason it takes a little while to load from SharePoint, but bear with it and it should come through.

Optimism Prism

The media is not a friend of the disciplined and patient investor. Ignoring the key determinants of lifetime investor returns, the media focuses on short-term returns, market predictions, and negative news.

We present the following as an antidote to the onslaught of negative news:

In Praise of Obsolescence: The Hidden Wealth in Products That Break

Google AI Tool That Fills Missing Words in Roman Inscriptions

Drones Carry 180 Tonnes of Steel and Concrete up Mountain

Recommendations

I’ve been playing about with ChatGPT quite a bit lately. I have the Teams version, but I believe the £20 a month Pro version would also help with this. Anyway, I recently created my own “GPT agent” (basically just by giving it a personality and explaining what I needed) and it’s worked really well. I asked it to draft workout plans for me, track progress, etc., and it is essentially like having a personal trainer in my pocket. Very cool. And ChatGPT 5 is on the way soon.

The PT’s name is Rebus, because why wouldn’t it be?

Speaking on Rebus (almost like that segway was intentional there), I recently watched the Netflix series with Richard Rankin in the main role, of course based on the superb Ian Rankin novels. Really enjoyed it – quite gritty, a bit rushed at times, but really good viewing for me and I think they nailed the casting. Looking forward to the next season already.

There’s a joke amongst IFAs that to be a real one you need to have a Tesla, a pizza oven, and a podcast. I’m currently on 0/3 and it looks like that will stay the way for a while, but we did recently get a breadmaker. Pretty handy so far, and nothing better than fresh bread and butter. That said, I’m sure it will be an ornament in three months.

That’s us for this month!

All the best,

Andy

This newsletter is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.

Past performance is used as a guide only; it is no guarantee of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

The value of investments and any income from them can fall as well as rise. You may not get back the full amount invested.

The Financial Conduct Authority (FCA) does not regulate Inheritance Tax Planning or Trust Advice.

Levels and bases of, and reliefs from, taxation are subject to change and their value will depend upon personal circumstances. Taxation and pension legislation may change in the future.